.png)

When Does Residual Value Become a Lender's Problem? (Earlier Than You Think)

For years, infrastructure lenders treated residual value as something that mattered later. Origination teams focused on sponsor quality, cash flow predictability, debt service coverage, and construction risk. Residual value was often reduced to a terminal assumption sitting quietly at the bottom of an underwriting model. Something relevant near maturity. Something future teams would deal with later.

That approach is starting to break. Across renewable energy, storage, and broader infrastructure debt markets, lenders are realizing that residual value risk in infrastructure lending does not suddenly appear at maturity. It begins much earlier, often years before the market notices. And by the time that risk becomes obvious, repricing the exposure is rarely easy.

The shift is happening because infrastructure assets are no longer aging in stable markets. Technology cycles are accelerating. Secondary market liquidity is becoming less predictable. Recovery pathways are changing. And the assumptions used during underwriting are increasingly diverging from real-world asset behavior. For lenders, that changes how infrastructure risk needs to be evaluated from day one.

Why Residual Value Risk Starts Earlier Than Most Lenders Think

The traditional infrastructure finance model assumed long-duration stability.

A solar farm, battery storage project, or energy infrastructure asset was expected to generate predictable cash flow over a 15 to 30-year lifecycle. As long as the project performed operationally, residual value concerns stayed in the background.

But operational stability does not eliminate collateral deterioration. This is where infrastructure residual value risk becomes difficult. A renewable asset can continue producing power while simultaneously losing recoverable market value underneath. Technology obsolescence, declining equipment pricing, repowering incentives, and shifting secondary demand all influence what that asset may realistically recover in the future.

Those changes often begin years before lenders adjust underwriting assumptions.

According to the International Energy Agency, solar module prices have declined more than 80% over the last decade. While that accelerated deployment globally, it also compressed future resale economics for aging assets. In many markets, replacing older systems with new technology now makes more financial sense than refurbishing aging infrastructure.

That directly impacts infrastructure asset recovery value. And it means lender exposure to aging infrastructure assets starts increasing long before maturity dates approach.

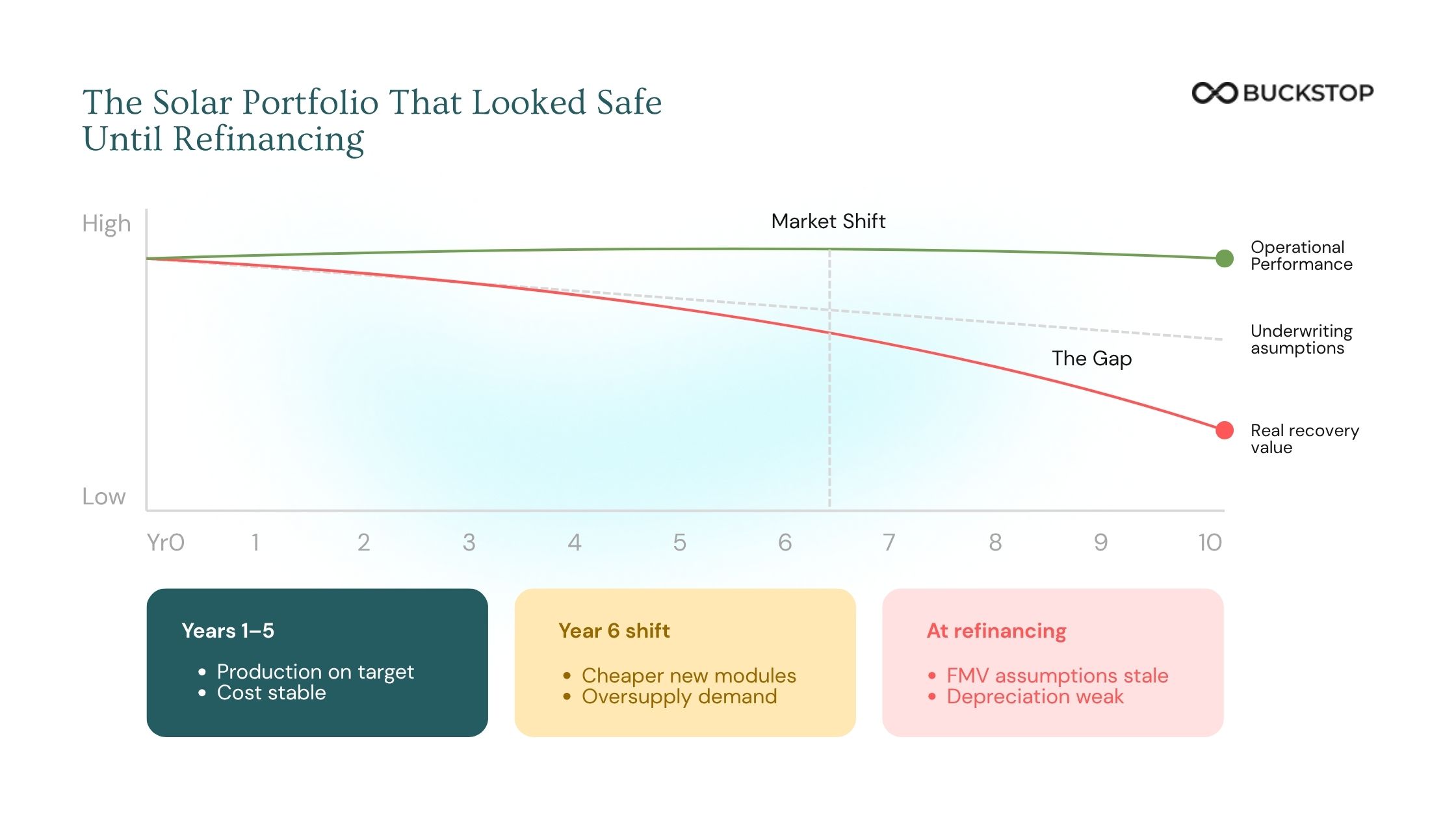

The Solar Portfolio That Looked Safe Until Refinancing

Consider a lender underwriting a 120 MW solar portfolio with a 10-year loan term. At origination, the deal looks strong.

- The sponsor has a solid track record

- The power purchase agreement is stable

- Debt service coverage looks healthy

- Independent engineering reports support the assumptions, and the underwriting model projects enough long-term fair market value in the equipment to support refinancing later in the asset lifecycle.

On paper, the collateral position appears secure.

For the first few years, the project performs exactly as expected. Production targets are met. Revenue stays predictable. The loan continues performing. Nothing looks wrong.

But by year six, the market surrounding the asset has changed materially. Newer solar modules have become significantly cheaper and more efficient. Buyers in secondary markets are showing less interest in aging equipment. Freight and dismantling costs have increased. Repowering the site with new technology now makes more economic sense than extending the life of the original infrastructure. Operationally, the project is still healthy. Financially, however, the infrastructure asset recovery value has started deteriorating underneath.

When refinancing discussions begin, the next lender is not evaluating the project based on the original underwriting assumptions from six years earlier. They are evaluating what the infrastructure could realistically recover in the current market. That changes the conversation quickly.

The original residual assumptions now appear optimistic. Expected fair market value no longer aligns with secondary market reality. Recovery economics look weaker after transportation, labor, recycling, and disposal costs are factored in. Importantly, nothing actually “failed.”

The sponsor did not default. The project continued generating power. Cash flows remained relatively stable. But the lender’s downside protection weakened years before maturity because the real-world recoverable value of the collateral moved faster than the underwriting model anticipated. This is exactly why residual value risk in infrastructure lending is becoming a much earlier-stage concern. The risk does not suddenly appear during default. It builds gradually while the asset is still operating normally.

Renewable Energy Collateral Risk Is No Longer a Late-Cycle Problem

Historically, many lenders assumed renewable energy collateral risk only became important during defaults or distressed scenarios. Today, it affects refinancing assumptions, portfolio valuations, and underwriting discipline much earlier in the asset lifecycle.

The reason is simple. Residual value assumptions are becoming harder to defend.

According to BloombergNEF, global clean energy investment exceeded $1.7 trillion in 2024, while utility-scale renewable deployment continues accelerating worldwide. But as deployment scales, so does the number of aging assets entering secondary markets simultaneously.

That creates pressure on long-term recoverability.

A lender underwriting a solar portfolio today is not just evaluating current operational performance. They are underwriting how that asset may compete in a future market flooded with newer, cheaper, and more efficient technology.

That changes energy infrastructure loan risk materially.

A project that appears stable from a cash flow perspective may still carry significant downside exposure if residual assumptions fail under refinancing or restructuring conditions.

This is one reason infrastructure credit markets are increasingly moving toward residual value underwriting for lenders rather than relying solely on traditional operational metrics.

Why Cash Flow Metrics Alone Are No Longer Enough

One of the biggest mistakes in infrastructure finance is assuming operational performance automatically validates collateral quality.

It does not.

A project can maintain strong debt service coverage while the underlying collateral value weakens underneath. Particularly in renewable infrastructure, where technology cycles move faster than traditional depreciation assumptions. This is becoming a major issue for lender exposure to aging infrastructure assets. Debt models often assume that if projects continue producing revenue, refinancing pathways remain available. But refinancing depends heavily on how future lenders assess infrastructure asset recovery value at that point in time.

If residual assumptions deteriorate materially, refinancing risk rises quickly. This is where residual value in project finance becomes central to underwriting strategy rather than a secondary consideration. The market is beginning to recognize that operational metrics alone cannot fully capture long-term downside protection. Because when infrastructure debt becomes stressed, the market does not evaluate the asset based on historical underwriting assumptions. It evaluates what the asset can realistically recover today.

Infrastructure Asset Recovery Value Is Becoming More Dynamic

One reason residual value risk in infrastructure lending is increasing is because recovery markets themselves are becoming more volatile. Ten years ago, lenders could rely on relatively predictable assumptions around equipment resale, secondary demand, and long-term infrastructure utilization.

Today, those assumptions are moving faster. Battery technology cycles continue shortening. Solar efficiency improvements continue accelerating. Recycling regulation is evolving across regions. Commodity pricing volatility impacts recovery economics directly. All of those factors influence infrastructure asset recovery value. This creates a difficult challenge for lenders because many underwriting frameworks still rely on static recovery assumptions spread across 15 to 25-year asset lifecycles. That approach increasingly misses real market behavior.

A lender may assume a portfolio retains 35% recoverable value at maturity while real-world market conditions suggest materially lower outcomes after dismantling, freight, labor, and disposal costs are incorporated. That gap is where renewable energy collateral risk becomes dangerous. Because once market conditions shift, collateral repricing can happen quickly.

How Buckstop Helps Lenders Evaluate Residual Value Risk Earlier

This is where Buckstop’s residual value intelligence becomes increasingly relevant for infrastructure lenders and project finance teams. Instead of treating residual value as a static assumption tied to depreciation schedules, Buckstop helps lenders evaluate how infrastructure assets may actually behave across resale, refurbishment, recycling, and recovery pathways. That distinction matters because residual value underwriting for lenders requires more than engineering assumptions or generalized recovery percentages.

It requires transaction-backed visibility into how real-world markets price aging infrastructure assets.

Buckstop helps infrastructure finance teams assess infrastructure residual value risk earlier in the underwriting lifecycle, before exposure becomes embedded inside portfolio assumptions. For lenders managing energy infrastructure loan risk, that means better visibility into how aging assets may impact refinancing, restructuring, and downside recovery scenarios over time. Because the firms adapting fastest are no longer asking whether residual value matters. They are asking how early residual deterioration becomes financially material to the portfolio.

The Future of Residual Value in Project Finance

Residual value in project finance is shifting from a back-end assumption to a front-end underwriting discipline.

As renewable infrastructure matures globally, lenders are under growing pressure to defend collateral assumptions with greater precision. LPs, insurers, infrastructure funds, and credit committees are increasingly asking harder questions around downside protection and recovery visibility.

That shift is changing infrastructure finance.

The next generation of infrastructure lenders will likely underwrite assets differently than the last decade. Operational performance will still matter. But so will understanding how technology evolution, secondary market liquidity, and recovery economics influence long-term collateral quality. Because ultimately, the biggest infrastructure risk is not always project failure. It is lenders discovering too late that the asset was worth materially less than the underwriting model assumed. And in today’s renewable infrastructure market, that realization is starting to happen much earlier than most lenders expected.

FAQs

What is residual value risk in infrastructure lending?

Residual value risk in infrastructure lending refers to the possibility that an infrastructure asset recovers materially less value than expected during refinancing, restructuring, or liquidation scenarios.

Why does residual value matter to lenders before loan maturity?

Residual value affects refinancing assumptions, collateral quality, and downside protection years before maturity. Deteriorating recovery economics can increase lender exposure long before operational problems appear.

How do lenders assess infrastructure asset recovery value?

Sophisticated lenders increasingly use transaction-backed recovery analysis that evaluates resale demand, refurbishment economics, recycling value, and secondary market conditions.

What causes renewable energy collateral risk to increase over time?

Technology obsolescence, declining equipment pricing, changing secondary market demand, disposal costs, and evolving recovery economics all contribute to increasing renewable energy collateral risk.

How does residual value affect project finance underwriting?

Residual value directly impacts collateral quality, refinancing assumptions, downside recovery potential, and long-term portfolio risk exposure.

Why are aging infrastructure assets becoming riskier for lenders?

As renewable assets age, they face growing pressure from newer technologies, falling replacement costs, and less predictable secondary market demand, reducing recoverable collateral value.

What is the difference between collateral value and residual value?

Collateral value often reflects modeled or accounting assumptions, while residual value reflects the asset’s actual recoverable market value under real-world conditions.

How can lenders reduce residual value underwriting risk?

Lenders can reduce risk by using transaction-backed residual value intelligence, scenario-based recovery modeling, and asset-level recovery analysis instead of relying solely on static depreciation assumptions.