.png)

The Cost of Getting End-of-Life Wrong in Infrastructure Finance

Infrastructure finance is built on long horizons and tight assumptions. Twenty-year cash flow models. Structured debt. Tax equity stacks. Predictable depreciation curves. But there is one line item that quietly drives more downside risk than most underwriting committees admit: terminal value.

More specifically, end-of-life risk in infrastructure and the residual value assumptions embedded inside it. When those assumptions are wrong, the consequences do not show up immediately. They surface at refinancing. At asset sales. At decommissioning. At bond maturity. And by then, the capital structure is already locked. This is where recovery value stops being theoretical and becomes a material balance sheet event.

The Hidden Variable in Infrastructure Finance: Terminal Value

In most models, terminal value infrastructure assumptions are treated as a residual number. A plug. A conservative haircut. Sometimes even zero. On paper, that feels prudent. In reality, it can be materially wrong in either direction. Infrastructure assets do not behave in straight lines:

- Commodity inputs fluctuate

- Secondary markets evolve

- Recycling and repurposing channels mature

- Regulatory frameworks shift

- Technology cycles shorten

Yet financial models often compress all that volatility into a static depreciation schedule or a fixed salvage percentage. That is not risk management. That is simplification. And simplification creates exposure.

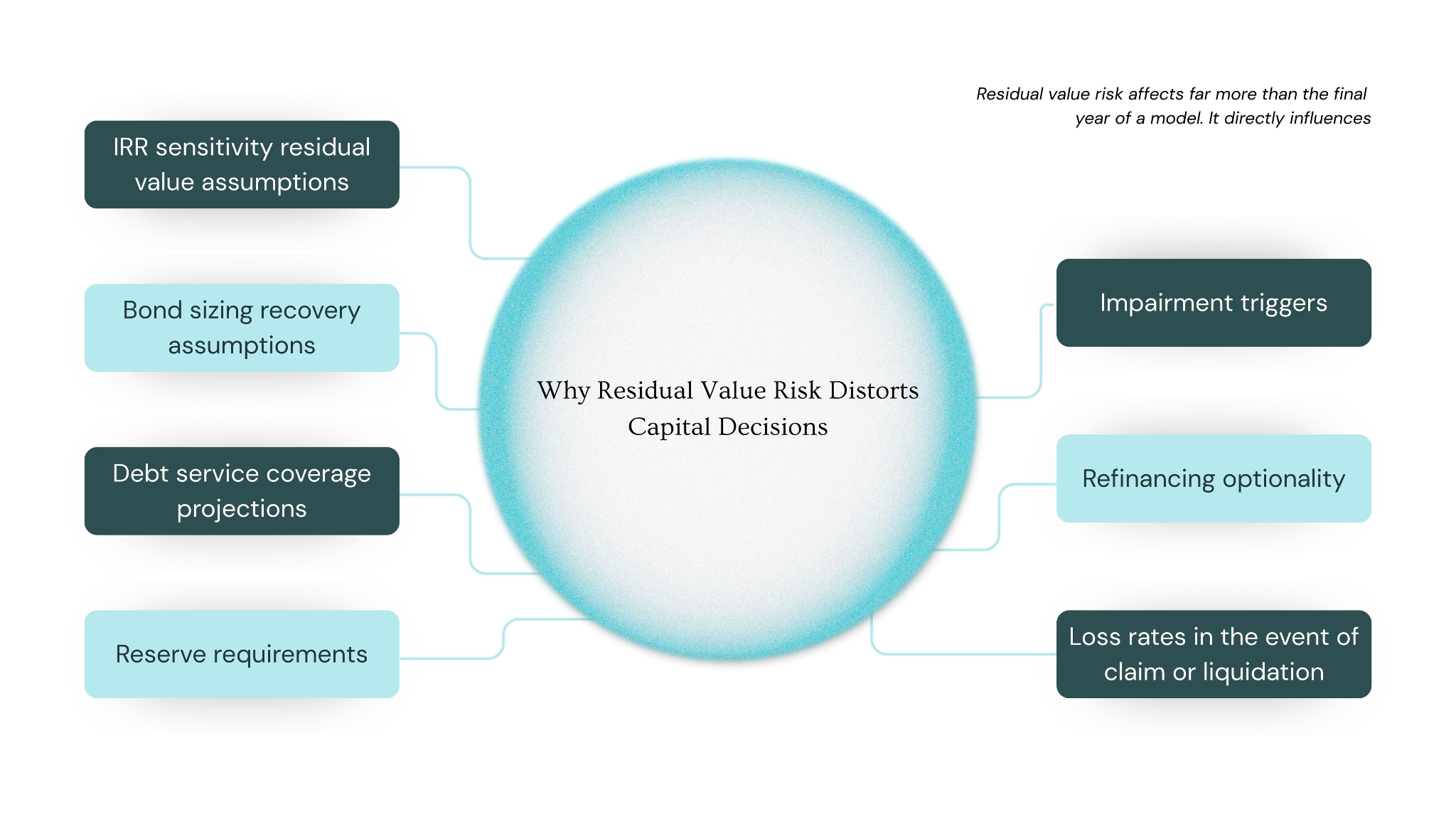

Why Residual Value Risk Distorts Capital Decisions

Residual value risk affects far more than the final year of a model. It directly influences:

- IRR sensitivity residual value assumptions

- Bond sizing recovery assumptions

- Debt service coverage projections

- Reserve requirements

- Impairment triggers

- Refinancing optionality

- Loss rates in the event of claim or liquidation

Consider a solar portfolio financed on 20-year PPA cash flows. If the model assumes minimal recovery value at year 20, debt sizing will be conservative. That may seem safe. But if the actual resale or recovery market supports meaningful value, capital has been inefficiently deployed. The opposite scenario is more dangerous.

If terminal value assumptions overstate recoverability, lenders and equity investors may discover at exit that the asset’s infrastructure finance recovery value is materially below modeled expectations. That delta hits equity first. Sometimes it cascades. The mistake is not that the future is uncertain. The mistake is pretending it is flat.

Book Value vs Market Value at End of Life

One of the most persistent modeling blind spots is the reliance on book value as a proxy for economic value. Book value is:

- Auditable

- Predictable

- Structured for accounting clarity

But it is not a market signal. At end of life, recovery value depends on:

- Asset composition and materials

- Component-level resale demand

- Scrap commodity pricing

- Transport and logistics economics

- Regional regulation

- Decommissioning pathways

- Secondary buyer networks

A straight-line depreciation schedule does not capture that. The divergence between book value vs market value becomes most visible when assets transition out of service. What looks clean on a balance sheet can translate into materially different outcomes in secondary markets. This is where downside risk in infrastructure assets accumulates quietly over time.

Decommissioning Risk Modeling Is Still Primitive

Despite the scale of global energy deployment, decommissioning risk modeling remains underdeveloped. Many models:

- Use static removal cost assumptions

- Apply uniform salvage percentages

- Ignore transaction-backed data

- Do not differentiate by asset class or vintage

- Fail to model volatility bands

The result is that end-of-life scenarios are often treated as administrative events rather than capital risk events. Yet in energy asset decommissioning, timing matters. Commodity markets can shift recovery economics within months. Landfill bans or recycling mandates can alter cost structures overnight. A surge in secondary demand can turn stranded assets into recoverable value streams. If your model does not incorporate market behavior, it cannot reflect recovery behavior. This is the gap Buckstop is built to address.

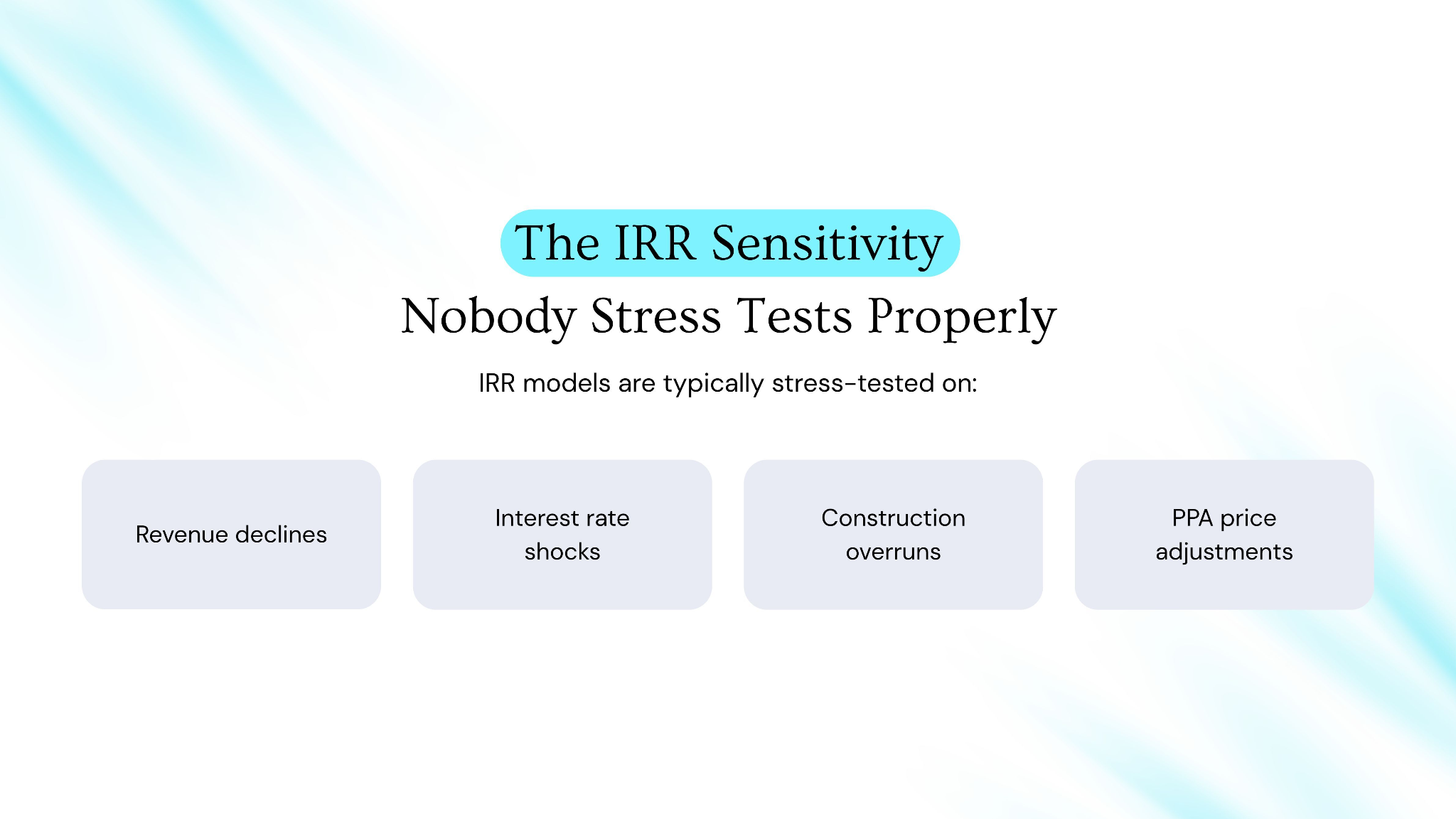

The IRR Sensitivity: Nobody Stress Tests Properly

IRR models are typically stress-tested on:

- Revenue declines

- Interest rate shocks

- Construction overruns

- PPA price adjustments

Residual value often receives minimal sensitivity treatment. When IRR sensitivity to residual value is not properly stress-tested, investors operate under false precision. The capital stack looks stable. The exit assumptions look reasonable. But the recovery scenario has never been validated against actual transaction data.

In other asset classes, recovery benchmarks exist. In automotive markets, more than 95 percent of vehicles are resold or recycled. Data informs underwriting. In energy and industrial infrastructure, recovery rates often struggle to reach even a fraction of that. And decision-makers still rely on assumptions rather than market-backed indices. That gap is measurable risk.

Bond Sizing and Capital Exposure

For lenders and structured finance participants, bond sizing recovery assumptions are critical. Overstated recovery values can:

- Inflate leverage tolerance

- Underprice credit risk

- Reduce required reserves

Understated values can:

- Constrain capital unnecessarily

- Reduce project competitiveness

- Increase weighted average cost of capital

Both distortions stem from the same root problem: insufficient decision-grade data on end-of-life behaviour. Infrastructure finance recovery value is not a theoretical construct. It influences covenant structures, impairment triggers, and refinancing outcomes. The cost of getting it wrong compounds across portfolios.

Why Static Assumptions No Longer Work

Infrastructure is transitioning into the later stage of its lifecycle, upgrades are accelerating, and new projects require the decommissioning of old ones. Assets are aging into secondary markets at scale for the first time. Solar, storage, and distributed energy portfolios are reaching maturity windows. Recycling supply chains are still forming. In this environment, static terminal value infrastructure assumptions are structurally outdated.

Financial models need:

- Transaction-backed benchmarks

- Component-level recovery visibility

- Commodity-linked sensitivity bands

- Scenario-based decommissioning outcomes

- Audit-defensible methodologies

This is not about forecasting the future with certainty. It is about replacing guesswork with evidence.

The Capital Discipline Shift

Institutional investors are increasingly asking harder questions:

- What data underpins your salvage assumptions?

- How do you validate recovery value?

- Are you modeling a range or a point estimate?

- What is your downside recovery floor?

- How do secondary markets affect exit optionality?

Answering those questions with static depreciation curves is no longer sufficient. End-of-life risk infrastructure exposure is moving from footnote to headline. The discipline is shifting from accounting-based proxies to market-based evidence.

From Assumption to Index

The difference between an assumption and an index is repeatability. Buckstop’s approach centers on building residual value benchmarks grounded in:

- Verified transaction data

- Asset-level technical documentation

- Observed resale and recovery behavior

- Market volatility calibration

Each index is launched only when sufficient transaction data supports defensible modeling. This moves infrastructure finance recovery value from a spreadsheet plug to a decision-grade input. When recovery value is grounded in market evidence:

- IRR sensitivity becomes transparent

- Bond sizing reflects realistic exposure

- Reserve planning aligns with actual risk

- Decommissioning strategy becomes proactive rather than reactive

The Real Cost of Getting It Wrong

The cost of misjudging end-of-life risk infrastructure exposure is rarely immediate. It shows up in:

- Unexpected impairment

- Refinancing friction

- Recovery shortfalls

- Reserve gaps

- Reduced investor confidence

- Capital inefficiency across portfolios

In a capital-intensive industry where margins are often measured in single digits, terminal value miscalculations can erase years of projected upside, leading to reduced investor confidence and potential losses for stakeholders. Infrastructure finance is built on long-term thinking. That thinking must now extend beyond operations into exit economics and recovery markets. Because at the end of every asset’s life, the question is no longer what it cost. The question is what it is actually worth. And that difference defines whether capital was protected or quietly exposed. Let's talk to the team if you have any questions about it.

Frequently Asked Questions

What is end-of-life risk in infrastructure finance?

End-of-life risk in infrastructure finance refers to the uncertainty around an asset’s recovery value when it exits service. It includes salvage value, resale potential, decommissioning costs, regulatory exposure, and market conditions at termination. If misjudged, it can distort IRR projections, debt sizing, and capital reserve planning.

Why is residual value risk important for infrastructure investors?

Residual value risk directly affects equity returns, bond sizing, and refinancing outcomes. A small change in terminal value assumptions can materially impact IRR in long-duration infrastructure projects. Without market-backed recovery benchmarks, investors may underestimate downside risk or misallocate capital.

How does terminal value affect IRR in infrastructure projects?

Terminal value is included in the final year cash flow of an infrastructure model. If recovery value is overstated, projected IRR appears higher than what the asset can actually deliver at exit. If understated, capital may be inefficiently structured. Proper IRR sensitivity analysis must stress-test residual value assumptions using transaction-backed data.

What is the difference between book value and market value at the end- -of-life?

Book value reflects accounting depreciation schedules. Market value reflects actual resale, recycling, or recovery demand. At end-of-life, these two values often diverge significantly. Relying on book value instead of market-based recovery benchmarks can misrepresent capital exposure.

How should decommissioning risk be modeled in energy infrastructure?

Decommissioning risk modeling should incorporate:

- Verified transaction data

- Commodity price sensitivity

- Asset composition analysis

- Secondary market demand

- Regulatory risk exposure

Static salvage percentages or flat depreciation curves are insufficient for decision-grade modeling.

How does residual value impact bond sizing and lender risk?

Bond sizing recovery assumptions influence leverage ratios and reserve requirements. Overstated recovery values increase lender exposure. Understated values can reduce capital efficiency. Accurate residual value modeling improves credit risk assessment and covenant structuring.

Why are residual value indexes becoming important in infrastructure finance?

Residual value indexes provide repeatable, market-backed benchmarks for recovery value. Instead of relying on assumptions, lenders and investors can reference transaction-based data. This reduces modeling error and improves capital protection across infrastructure portfolios.