.png)

Portfolio-Level Residual Value: How Infrastructure Funds Are Rethinking Exit Risk

Infrastructure funds used to treat residual value as a footnote in the underwriting model. A terminal multiple, a recovery curve, a placeholder assumption pulled from a 2018 deck. That era is over. With holding periods stretching past 10 years, energy transition assets reshaping portfolios, and LPs asking sharper questions about downside protection, portfolio residual value has moved from afterthought to underwriting cornerstone.

The funds pulling ahead right now are the ones treating infrastructure asset residual value as a live, data-driven discipline. Not a static line item. Not a single recovery percentage applied across a 14-asset portfolio. A defensible, transaction-backed view of what each asset is actually worth at exit, and how that value behaves across stress scenarios. What used to sit in a terminal value input is becoming central to infrastructure portfolio risk management.

This piece breaks down how leading GPs are restructuring their approach, what tools they are using, and where most funds are still leaving 200 to 600 basis points of IRR on the table.

McKinsey has estimated infrastructure as an asset class could require trillions in capital through the energy transition over coming decades, while market volatility and rising financing costs have made downside protection far more scrutinized. In that context, even a 10%-15% shift in recovery assumptions can materially affect portfolio returns. That is why residual value risk in infrastructure investing is moving higher on investment committee agendas.

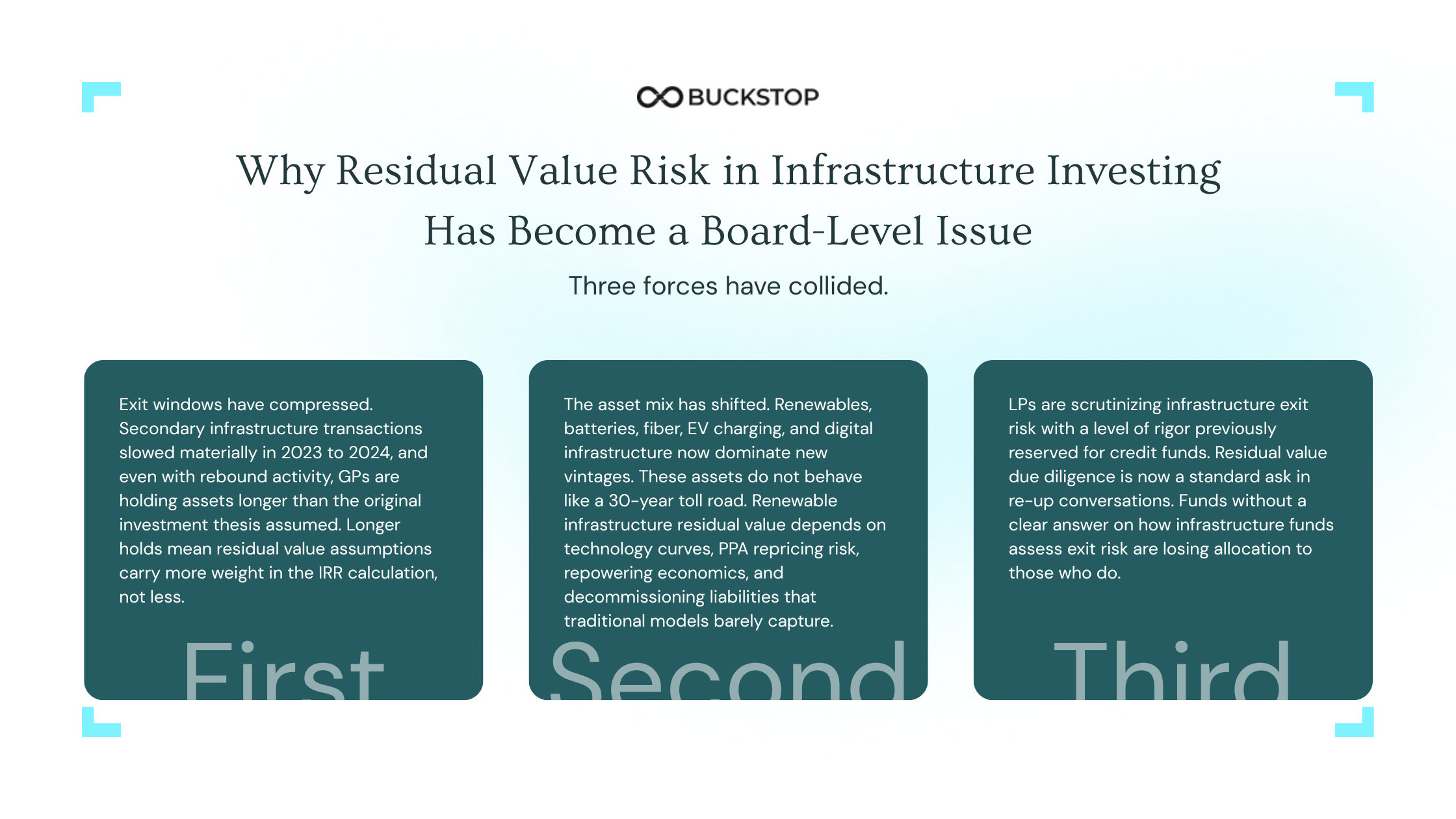

Why Residual Value Risk in Infrastructure Investing Has Become a Board-Level Issue

Three forces have collided.

First: Exit windows have compressed. Secondary infrastructure transactions slowed materially in 2023 to 2024, and even with rebound activity, GPs are holding assets longer than the original investment thesis assumed. Longer holds mean residual value assumptions carry more weight in the IRR calculation, not less.

Second: The asset mix has shifted. Renewables, batteries, fiber, EV charging, and digital infrastructure now dominate new vintages. These assets do not behave like a 30-year toll road. Renewable infrastructure residual value depends on technology curves, PPA repricing risk, repowering economics, and decommissioning liabilities that traditional models barely capture.

Third: LPs are scrutinizing infrastructure exit risk with a level of rigor previously reserved for credit funds. Residual value due diligence is now a standard ask in re-up conversations. Funds without a clear answer on how infrastructure funds assess exit risk are losing allocation to those who do.

McKinsey has estimated infrastructure as an asset class could require trillions in capital through the energy transition over coming decades, while market volatility and rising financing costs have made downside protection far more scrutinized. In that context, even a 10%-15% shift in recovery assumptions can materially affect portfolio returns. That is why residual value risk in infrastructure investing is moving higher on investment committee agendas.

Why Asset-Level Models Miss Portfolio Risk

Traditional asset residual value modeling for infrastructure portfolios often relies on depreciation schedules and static exit assumptions. But infrastructure assets do not exit in static markets. Commodity prices move. Secondary demand changes. Repowering economics evolves. Regulation shifts. Recovery channels tighten.

That is why residual value forecasting for infrastructure assets has become more scenario-driven. Take two similar energy assets. Same vintage. Similar operating history. One exits in a strong secondary resale market. Another is forced through scrap recovery. Recovery outcomes can differ by 30%-40%. That is not noise. That is exposure.

This is where market-based residual value and transaction-backed residual value approaches are reshaping underwriting. Investors are supplementing traditional models with observed recovery outcomes, not just modeled depreciation. That shift improves portfolio underwriting risk analysis and strengthens how infrastructure funds assess exit risk.

Asset-Level vs Portfolio-Level Residual Analysis: The Gap Most Funds Miss

Most funds still run residual value bottom-up. Each asset gets its own terminal value assumption, and the portfolio number is just the sum. This misses the entire point of portfolio-level residual value analysis.

Real portfolio valuation risk lives in the correlations. When power prices crater, your solar farm in Texas, your battery storage in Arizona, and your gas peaker in Oklahoma all reprice at the same time. When interest rates spike 200 bps, every transmission asset in your book gets re-rated simultaneously. Asset-level models miss this. Portfolio-level residual value scenario analysis captures it.

The funds doing this well are running three layers in parallel:

- Asset residual value modeling for infrastructure portfolios at the individual deal level, with residual value forecasting for infrastructure assets built on transaction comps rather than DCF projections alone.

- Recovery value modeling that maps multiple recovery pathways for each asset: strategic sale, secondary fund sale, IPO, refinance, partial divestiture, or in worst-case scenarios, decommissioning risk assessment and end-of-life asset valuation.

- Portfolio liquidation risk stress tests that model what happens when three of your top five exits hit simultaneous market headwinds.

This is what decision-grade residual value intelligence actually looks like in practice.

How Investors Price Recovery Value in Infrastructure Today

The methodology gap between best-in-class and median funds is wide.

Median funds use a single point estimate for terminal value, often anchored to entry multiple plus some inflation. Best-in-class funds build market-based residual value distributions using transaction-backed residual value data, then layer in decommissioning economics, repowering optionality, and infrastructure asset recovery value under multiple macro scenarios.

The difference shows up in infrastructure fund returns. Funds with structured residual value processes have outperformed peers by roughly 180 to 240 bps net IRR over recent 10-year vintages. Improving infrastructure fund returns through residual value intelligence is no longer a hypothesis. It is a measurable edge.

Key inputs the leaders are pulling in:

- Live secondary market transaction data for comparable asset exit valuation models

- Technology obsolescence curves for renewable, digital, and storage assets

- Counterparty credit migration data affecting collateral risk in infrastructure finance

- Regional regulatory shift modeling, especially around grid interconnection and permitting

- Liquidation value risk benchmarks across asset class and vintage

The New Underwriting Stack for Infrastructure Portfolios

Underwriting infrastructure portfolios without a residual value layer is now considered incomplete. Here is the structure top-decile funds are using:

Pre-investment. Residual value due diligence before capital deployment runs in parallel with commercial DD. Teams validate residual value assumptions against transaction comps, not just internal DCF outputs. They benchmark recovery value assumptions across at least three independent data sources. Post-close, ongoing. Infrastructure portfolio risk management treats residual value as a quarterly metric, not an annual one. Residual value uncertainty gets quantified and reported to LPs the same way mark-to-market does in credit funds.

Pre-exit. Portfolio recovery scenario modeling runs 18 to 24 months before any planned divestiture. This is where portfolio underwriting risk gets re-tested against current market conditions, and where most value leakage actually happens for funds without a structured process. This stack is what produces defensible residual value assumptions, the kind that hold up in IC, in LP meetings, and in audit.

Recovery Pathways Are Becoming a Core Valuation Input

A major change in how investors price recovery value in infrastructure is the move away from one-number residual assumptions. Assets have pathways, not one exit. And those pathways matter.

Especially in residual value models for solar and energy assets, where reuse, refurbishment, repowering and recycling economics can materially alter outcomes. This is where decommissioning risk assessment intersects with value. And why stronger end-of-life asset valuation practices are becoming part of underwriting.

Investors focused on how to reduce downside risk in infrastructure portfolios are looking more closely at:

- recovery channel liquidity

- secondary market depth

- commodity-linked downside

- policy exposure

- asset-specific recovery optionality

This is not theoretical. For many funds, improved recovery assumptions can move downside IRR sensitivity by meaningful percentages. That is why improving infrastructure fund returns through residual value intelligence is becoming less about optimization and more about avoiding mispriced risk.

Where This Is Heading

Residual value models for solar and energy assets are evolving fast. Battery degradation curves, repowering economics, and second-life value are becoming standard inputs. Recovery pathway valuation is moving from spreadsheet exercise to dedicated platform discipline.

The funds that figure this out first will price deals more accurately, win more secondary auctions, and report cleaner IRRs to LPs. The ones that do not will keep absorbing surprises at exit and explaining them in quarterly letters. How to assess exit risk in infrastructure portfolios is no longer a niche capability. It is core infrastructure investing.

Questions Funds Should Ask Before Capital Is Committed

Before deploying capital, investors should pressure test:

- Are we using robust residual value models for solar and energy assets, or static depreciation proxies?

- How much of our downside case depends on untested recovery assumptions?

- Have we run portfolio-level residual value analysis across correlated exposures?

- Do our assumptions reflect market-based residual value signals?

- Where does hidden portfolio underwriting risk sit in the portfolio?

- Are we using residual value assessment as part of underwriting, or only near exit?

These questions increasingly define risk discipline. Not just valuation discipline.

The Shift Ahead

The firms getting ahead are not treating portfolio residual value as a terminal assumption anymore. They are treating it as a strategic lens for risk. That changes how they underwrite.

- How they allocate capital

- How they protect return.

- And ultimately, how they manage infrastructure asset residual value across a portfolio

Because residual value risk in infrastructure investing is no longer a niche modeling issue. It is a portfolio issue. And increasingly, a competitive advantage for those who understand it better.

If your team is looking to run a portfolio exposure review, strengthen residual value due diligence, or explore how infrastructure funds assess exit risk using transaction-backed recovery intelligence, Buckstop can help you benchmark assumptions before those assumptions get tested by the market.

FAQs

What is portfolio residual value?

Portfolio residual value refers to the aggregate recovery value potential and residual exposure across a portfolio of infrastructure assets, rather than evaluating assets individually. It helps investors assess concentration risk, downside exposure and exit resilience.

Why are infrastructure funds rethinking exit risk?

Many funds are rethinking infrastructure exit risk because static residual assumptions often miss market volatility, recovery uncertainty and correlated portfolio exposure. Scenario-based residual analysis improves downside protection.

How do infrastructure funds model residual value risk?

Leading firms use asset residual value modeling for infrastructure portfolios, recovery value modeling, stress testing, transaction-backed data and portfolio recovery scenario modeling to assess risk under multiple exit conditions.

Why does residual value due diligence matter before capital deployment?

Residual value due diligence before capital deployment helps investors validate assumptions early, improve underwriting decisions, reduce collateral risk in infrastructure finance, and avoid mispriced downside exposure.

How can residual value intelligence improve infrastructure fund returns?

By improving recovery assumptions, identifying hidden risk, and strengthening infrastructure fund downside protection, residual value intelligence for infrastructure funds can support better risk-adjusted returns.

What should investors review before making a high-stakes infrastructure decision?

Investors should benchmark recovery value assumptions, stress test portfolio exit risk, review decommissioning risk assessment, and use decision-grade residual value intelligence to validate assumptions before capital is committed.