.png)

Statement of Values for Solar Assets: What to Include and How to Get It Right

A statement of values for solar assets is the document that determines how much insurance you can actually collect when something goes wrong. Not the policy limit. Not the declared TIV. The actual recoverable amount at the time of loss, which is a function of how accurately your SOV reflects what your assets are worth at that moment, not when the document was last prepared.

Most solar project owners, developers, and asset managers treat the statement of values as an administrative exercise. Submit it at policy inception, index-link it annually, and revisit it when the insurer asks a question. That approach worked in a market where module prices were stable, commodity values moved slowly, and underwriters had wide tolerances for valuation imprecision.

That market no longer exists. And the financial consequences of an inaccurate statement of values for solar assets in 2026 are more direct and more immediate than most teams have accounted for.

What a Statement of Values Is and What It Actually Does

A Statement of Values is a formal document submitted to an insurer that lists every insured property, its declared value, and the basis on which that value was determined. For utility-scale and commercial solar assets, it is the primary input into every financial instrument that depends on asset valuation: the total insured value, the policy premium, the coverage limit, and the maximum payout available in the event of a covered loss. It is not a summary but a a valuation document, and it carries legal and financial weight that most practitioners underestimate, until a loss event makes the gap visible.

Solar property insurance valuation built on an SOV that was accurate at financial close but never updated is not a current SOV. It is a historical record that happens to be attached to an active policy. When a loss occurs, the insurer assesses the claim against the actual replacement cost at the time of loss, not the declared value at the time of binding. If the declared value is below the actual replacement cost, a coinsurance clause triggers a proportional reduction in the payout.

A coinsurance clause in commercial property insurance sets a minimum amount of insurance you are expected to carry, typically 80%, 90%, or 100% of the property's replacement cost. If your limit falls short of that requirement, the carrier may only pay part of an otherwise covered loss, even when the loss itself is fully covered. (Reasons Insurance, November 2025)

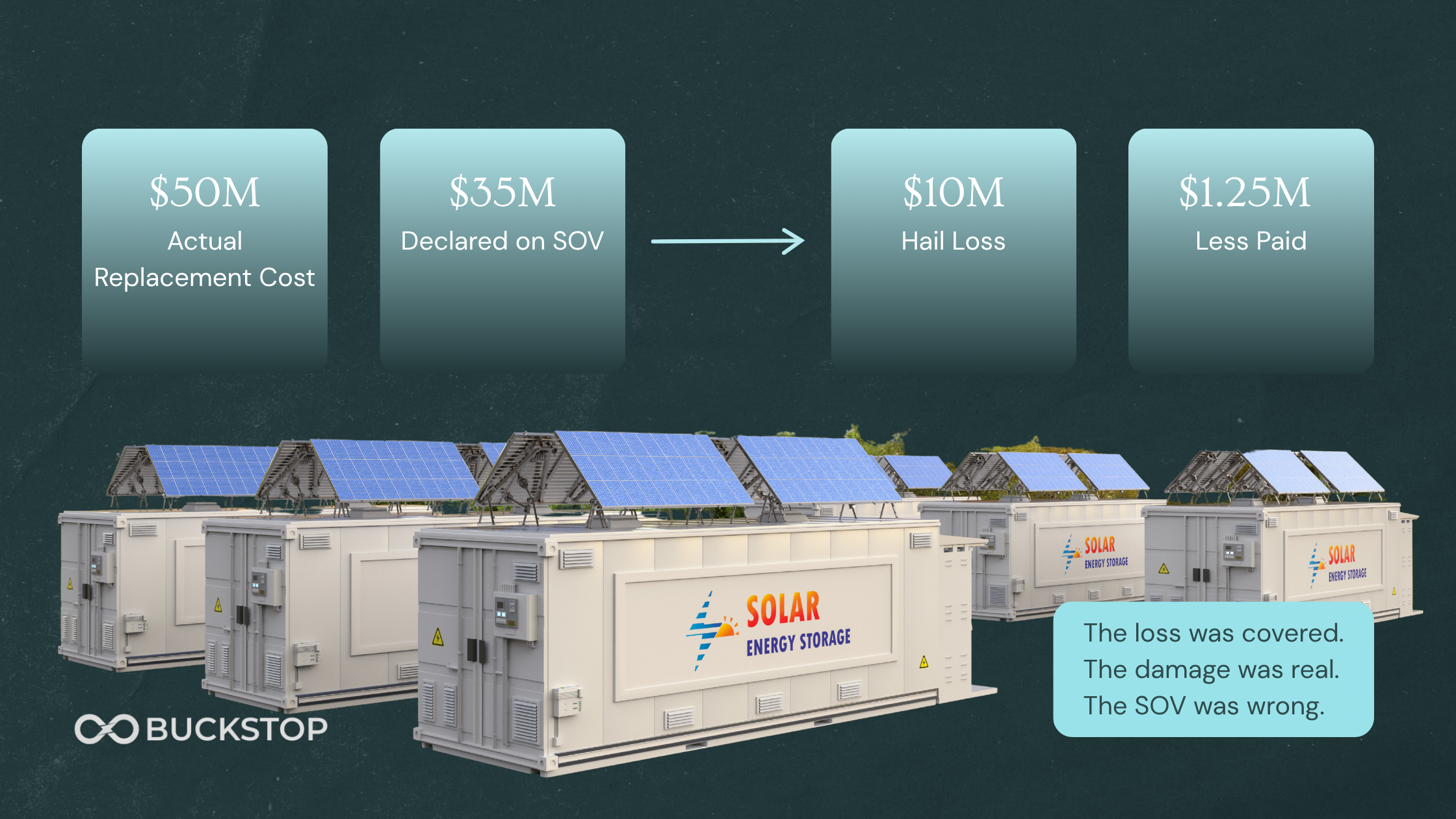

For a utility-scale solar project with $50 million in actual replacement cost and an SOV declaring $35 million, the coinsurance penalty on a $10 million hail loss at 80% coinsurance would reduce the payout by approximately $1.25 million. The loss was covered. The damage was real. But the claim was reduced because the SOV was wrong.

Severe convective storms drove $60 billion in insured losses in 2025, the third-costliest SCS year on record for insurers. Hail accounted for just 6% of loss incidents but 73% of financial losses at solar farms. (PV Magazine, May 2026 / Renew Risk via Insurance Edge, May 2026) The probability of a loss event that triggers this clause is not theoretical. It is the primary risk driver in the US solar insurance market right now.

What Must Be Included in a Statement of Values for Solar Assets

A complete and defensible statement of values for solar assets at the utility-scale or large C&I level must cover seven distinct asset categories, each requiring specific data inputs that are more granular than most current SOV processes capture.

1. Solar Modules

Module data must include manufacturer, model, technology type, wattage, quantity, vintage year, and current condition rating. Replacement cost must reflect current market pricing for that specific technology type under current tariff conditions, not project cost at financial close.

This distinction is material in 2026. Antidumping and countervailing duties of up to 3,521% on solar imports from Cambodia, Vietnam, Malaysia, and Thailand, which together represented 77% of total US module imports, have materially changed the replacement cost economics for the majority of modules currently in the field. (US Department of Commerce, April 2025) A module specified in 2021 at $0.25 per watt may cost $0.285 to $0.33 per watt to replace today depending on technology type and FEOC compliance requirements. An SOV built on original procurement costs is systematically understated.

2. Inverters

Inverter data must include manufacturer, model, capacity in kW or MW, quantity, vintage, and current condition. Replacement cost should account for current manufacturer pricing, supply chain lead times, and technology generation. String inverter, central inverter, and microinverter replacement costs vary significantly and should not be aggregated.

Inverter shutdowns drive 28% of recoverable solar performance risk across 6.5 GW of analyzed assets. (kWh Analytics, May 2026) Inverters are both the most likely component to require replacement and one of the most variable in replacement cost terms. An SOV that uses a generic per-watt inverter replacement figure without capturing manufacturer-specific pricing and current lead time assumptions is producing an inaccurate replacement cost for the single most likely claim component. Precedence Research

3. Racking and Mounting Systems

Fixed-tilt and tracker systems carry materially different replacement costs, different labor requirements, and different supply chain profiles. Single-axis tracker systems have become the dominant configuration for utility-scale solar, representing over 80% of new US utility-scale capacity in recent years. Tracker replacement costs include not just the mechanical components but the motor systems, control electronics, and calibration labor that fixed-tilt systems do not require. The SOV must distinguish between these system types and apply appropriate replacement cost inputs to each.

4. Transformers and Electrical Balance of Plant

Transformer lead times extended to 18 months or longer during 2023 and 2024 due to supply chain constraints and grid modernization demand that created a structural backlog. While lead times have moderated somewhat, transformer replacement remains one of the highest-risk BI exposure items in a solar SOV. The replacement cost for transformers must reflect current equipment pricing and the BI exposure from extended replacement timelines must be captured in the business interruption section of the SOV.

5. BESS Components

For projects with battery energy storage, the SOV must capture battery modules by chemistry, manufacturer, model, capacity in MWh, vintage, state of health, and current cycle count. Power conversion systems, HVAC systems, fire suppression systems, and battery management systems must be captured separately.

LFP battery systems typically receive more favorable insurance rates than NMC systems due to lower thermal runaway propagation risk. Most insurers now require detailed documentation of battery management systems, thermal management protocols, and emergency response procedures before providing coverage for BESS assets. (Solarif, January 2026) The SOV must include this documentation to support underwriting, and the replacement cost figures must reflect battery chemistry-specific pricing. NMC replacement cost is more sensitive to nickel and cobalt commodity movements. LFP replacement cost is more sensitive to lithium and iron phosphate pricing.

6. Civil and Site Infrastructure

Access roads, fencing, foundations, conduit, and site preparation infrastructure are frequently underrepresented in solar SOVs. Their replacement cost is driven by current labor rates in the project's geography, current material costs, and current permitting timelines. For projects in states with significant labor cost variation or in regions experiencing elevated construction activity, the civil infrastructure replacement cost can represent a meaningful share of total SOV value that generic assumptions systematically understate.

7. Business Interruption Values

Business interruption and delay in start-up exposures are expected to increase in 2026 as aging transmission equipment and increased congestion create longer and more frequent outages, and data centers amplify local grid stress. (NARDAC, December 2025) BI values in the SOV should be based on current revenue projections, current replacement timelines for critical components, and current grid interconnection conditions at the project location. BI values set at financial close and never updated carry the same systematic inaccuracy as replacement cost figures that have not been refreshed.

The Five Most Common SOV Errors in Solar Projects

Understanding where statement of values preparation typically goes wrong is as important as knowing what to include.

Error 1: Using original equipment cost rather than current replacement cost

Solar insurance replacement cost value is not historical cost. It is what it would cost to replace the asset at current market prices, in its pre-loss condition, under current tariff and supply chain conditions. US module prices moved 14% in a single year between January and November 2025. A replacement cost figure that does not reflect current pricing is not a replacement cost figure. It is a procurement record.

Error 2: Applying system-level per-watt estimates rather than component-level pricing

A single per-watt replacement cost figure applied across an entire project smooths over component-level variation that is financially material. Mono PERC modules hit $0.33 per watt in February 2026. TOPCon modules were at $0.285 per watt in the same period. Fixed-tilt racking carries different replacement economics than single-axis trackers. NMC and LFP battery systems carry different replacement costs and different insurance risk profiles. System-level averaging produces a number that accurately describes none of the individual components it covers.

Error 3: Omitting salvage value from the net cost calculation

Solar salvage value calculation is not a decommissioning concern alone. It directly affects the net replacement cost figure and, in states where financial assurance requirements mandate that bond amounts equal decommissioning cost minus salvage value, it also affects bond sizing. Copper hit a record $14,527 per metric ton in January 2026. Silver gained more than 130% during 2025 and reached an all-time high above $121 per ounce. (Crux Investor, March 2026 / Investing News Network, April 2026) The metallic content of a utility-scale solar asset is worth materially more today than any pre-2025 salvage assumption reflects. An SOV that ignores this overstates net replacement cost and generates excess premium.

Error 4: Failing to update the SOV when the asset composition changes

Repowering, equipment replacements, additions, and condition changes all affect the accuracy of the SOV. US solar is on track to add a record-breaking 86 GW of new utility-scale capacity in 2026. (Renew Risk via Insurance Edge, May 2026) Many of those projects will involve hybrid configurations combining solar and BESS that did not exist when the original SOV framework was built. An SOV that was accurate for a solar-only asset does not automatically capture the additional complexity and replacement cost of an added BESS system.

Error 5: Missing the 25% valuation step-up threshold

75% of renewable energy tax insurance underwriters will not cover valuation step-ups above 25%. (kWh Analytics via CAC, May 2026) If an SOV needs to be corrected upward by more than 25% at renewal to reflect actual current replacement cost, it is not simply a matter of submitting a revised figure. The majority of the underwriting market will not accept the corrected value without additional scrutiny, and in some cases will decline to provide coverage at the corrected level entirely. The practical consequence is that a stale SOV does not just create underinsurance risk at claims time. It creates access problems at renewal time.

How Salvage Value Connects the SOV to Decommissioning and Financing

The statement of values for solar assets, the decommissioning bond, and the collateral assessment in a project finance facility are three separate documents that share one underlying dataset: the asset-level valuation of what is in the field and what it would recover under different scenarios.

Most project teams treat these as separate workstreams handled by different advisors at different points in the project lifecycle. The SOV is prepared at financial close by the insurance broker. The decommissioning bond is sized by a consultant at permitting. The collateral valuation is assessed by the lender at underwriting.

In practice, a salvage value error made in one document propagates into all three. An understated salvage assumption in the decommissioning plan produces an oversized bond requirement, locking up capital unnecessarily for decades. The same understated salvage assumption in the SOV overstates net replacement cost and inflates the premium. And the same assumption in the collateral assessment understates the recovery value available to the lender in a distress scenario.

Accurate solar asset replacement cost calculation requires transaction-backed salvage benchmarks built from real observed outcomes across resale, refurbishment, recycling, and scrap pathways. Not a percentage assumption. Not a comparable-site estimate. Observed market data that reflects what comparable assets are actually recovering under current commodity prices, secondary market demand, and technology cycle conditions.

More than 35 states now have statewide solar decommissioning policies, and more than half of all US states had legislative action on solar and storage decommissioning in 2025, double the number from 2024. (NC Clean Energy Technology Center, January 2026) The legal requirement for decommissioning bonds in the majority of US states means the salvage value assumption in your SOV is not just an insurance issue. It is a regulatory and financial planning issue that has real capital consequences.

What Utility-Scale Solar Insurance Requirements Mean for SOV Preparation in 2026

The utility-scale solar insurance requirements that underwriters are applying in 2026 are more specific and more data-intensive than anything the market required three years ago.

Structured data is no longer a differentiator for insurers. It is a requirement. (NARDAC, December 2025) An underwriter reviewing a solar SOV submission today is looking for documentation that most legacy processes are not set up to provide.

For property coverage, underwriters want component-level asset inventories rather than system-level specifications, current market pricing sources with stated update dates, and methodology documentation that explains how replacement cost figures were derived. A per-watt estimate with no supporting data is not adequate for a market where 75% of underwriters will not cover valuation step-ups above 25%.

For BESS coverage, underwriters additionally require battery management system certifications, thermal management protocol documentation, fire suppression system specifications, emergency response procedures, and state of health data where available. Fire risk remains the dominant underwriting concern for BESS, with one underwriter describing the challenge as calibrating on both technology risk and climate trajectory simultaneously with very thin data on either. (Repath.earth, March 2026) An SOV that treats BESS components as a line-item addition to a solar SOV without capturing this additional documentation will not meet current underwriting requirements at most specialty carriers.

For business interruption coverage, underwriters are increasingly focused on supply chain lead times and grid interconnection risk. In solar, grid-originating outages were one of the biggest BI cost drivers of 2024 and 2025, with delay in start-up, business interruption, and contingent business interruption exposures remaining major underwriter concerns in 2026. (NARDAC, December 2025) BI values that do not account for current transformer lead times, current inverter availability, and current grid congestion conditions in the project's ISO or RTO are systematically understated.

How Buckstop Approaches Solar Asset Valuation for SOV Purposes

Buckstop builds transaction-backed residual value intelligence for solar and BESS assets across every recovery pathway including resale, refurbishment, recycling, liquidation, and scrap.

The methodology is built on observed market data tied to actual recovery outcomes rather than static percentage assumptions or comparable-site estimates. It accounts for manufacturer, age, wattage, condition, configuration, and geographic and regulatory factors that influence both replacement cost and recovery value. Commodity price movements, secondary market transaction data, and technology-specific pricing are incorporated on an ongoing basis rather than captured once and held static. Buckstop platform methodology.

For SOV preparation purposes, this means the salvage value inputs and net replacement cost figures that go into a statement of values for solar assets can be supported by transaction-backed data rather than assumptions. That matters not just for accuracy but for defensibility. When an underwriter asks where the salvage value figure came from, the answer needs to be observed market transactions, not a consultant's estimate from three years ago.

The Bottom Line

A statement of values for solar assets is only accurate on the day it is prepared against current market data. Every day after that, the market moves and the SOV does not. In a market where module prices moved 14% in a single year, commodity prices are at multi-year or all-time highs, and tariff conditions have fundamentally changed the cost of replacing the majority of modules currently in the field, the gap between a stale SOV and an accurate one widens faster than at any previous point in this asset class's history.

The global solar plant insurance market generated $5.6 billion in premiums in 2024 and is projected to reach $13.8 billion by 2034. (Market.us, October 2025) The scale of financial exposure behind those premium dollars makes the accuracy of the underlying SOV not a documentation concern but a risk management priority.

The teams getting solar SOV preparation right in 2026 are the ones treating it as a live data problem. Component-level inventory. Current market pricing. Transaction-backed salvage benchmarks. Documented methodology with a stated update date. Those are the inputs that produce a statement of values that holds up when a loss occurs, when an underwriter scrutinizes a renewal, and when a lender asks what the collateral actually recovers.

Buckstop builds transaction-backed residual value intelligence for solar and BESS assets across resale, refurbishment, recycling, liquidation, and scrap pathways. Explore Buckstop Residual Value Intelligence

Frequently Asked Questions

What is a statement of values for solar assets?

A statement of values for solar assets is a formal document submitted to an insurer that lists all insured components of a solar project, their declared values, and the valuation methodology used to determine those values. It is the primary input into the total insured value calculation and determines the coverage limit, policy premium, and maximum payout available in the event of a covered loss. For utility-scale solar, it typically covers modules, inverters, racking and mounting systems, transformers, BESS components, balance of plant, civil infrastructure, and business interruption values.

What is the difference between replacement cost value and actual cash value for solar assets?

Solar insurance replacement cost value covers the cost to replace an asset at current market prices in its pre-loss condition without deducting for depreciation. Actual cash value deducts depreciation from replacement cost. Replacement cost is the more commonly used basis for utility-scale solar because it provides full coverage for asset replacement rather than a depreciated value that may be significantly below actual replacement cost. For older assets, the gap between ACV and current replacement cost can be material given that module prices, tariff conditions, and labor costs have all moved since most projects were built.

What happens if a solar SOV understates actual replacement cost?

If a solar SOV understates actual replacement cost, two things happen. First, if the policy has a coinsurance clause requiring coverage at 80%, 90%, or 100% of actual replacement cost, any shortfall triggers a proportional reduction in claim payouts even for fully covered losses. Second, if the SOV needs to be corrected upward by more than 25% at renewal, 75% of renewable energy tax insurance underwriters will not cover the step-up, creating coverage access problems rather than just premium adjustment. The coinsurance penalty applies at the time of loss based on actual replacement cost at that moment, not at the time the policy was bound.

How often should a solar statement of values be updated?

Given current market conditions, annual updates reflecting current module pricing by technology type, current tariff-inclusive replacement costs, current commodity values for salvage offset calculations, and current supply chain lead times for BI values are the minimum appropriate standard. US module prices moved 14% in a single year. Copper rose 16% in a single month in early 2026. A statement of values that is indexed to general inflation rather than asset-specific market pricing will diverge from actual replacement cost at a rate that creates meaningful financial exposure over a two to three year period.

What data is needed for BESS components in a solar SOV?

BESS components in a solar statement of values require battery module data by chemistry, manufacturer, model, capacity, vintage, and state of health. Power conversion systems, HVAC systems, fire suppression systems, and battery management systems must be captured separately. Most insurers now require thermal management protocol documentation, BMS certifications, and emergency response procedures as part of the underwriting package for BESS coverage. LFP and NMC systems carry different replacement cost profiles, different risk profiles, and different underwriting requirements and should not be aggregated in the SOV.

How does solar salvage value affect the statement of values?

Solar salvage value is a direct offset against net replacement cost in the SOV calculation and against decommissioning bond sizing in states with financial assurance requirements. An accurate salvage value reduces both the net TIV and the required bond, freeing up capital. Copper above $13,000 per metric ton and silver at an all-time high mean that current metallic content values are materially above what pre-2025 salvage assumptions reflect. An SOV that uses an outdated salvage assumption overstates net replacement cost, inflates the premium, and produces a decommissioning bond that locks up more capital than the asset's actual net liability requires.

What does a defensible solar SOV look like to an underwriter in 2026?

A defensible solar statement of values in 2026 includes component-level asset inventory verified against actual deployed equipment, current market pricing by technology type with stated sources and update dates, transaction-backed salvage value benchmarks supported by recent secondary market data, BI values based on current supply chain lead times and revenue assumptions, BESS-specific documentation meeting current insurer requirements, and clear methodology documentation. The 75% of renewable energy tax insurance underwriters who will not cover valuation step-ups above 25% are specifically looking for this level of rigor before accepting a corrected SOV submission.