.png)

Solar Decommissioning Bonds & TIV: The Connection Most Lenders Are Missing

Total insured value for renewable energy assets and solar decommissioning bonds are treated by most lenders, insurers, and asset owners as separate financial instruments managed by separate teams at separate points in the project lifecycle. They are not separate. They are built from the same underlying dataset. And the errors embedded in that dataset propagate simultaneously into both instruments in ways that create real financial exposure across the life of the project.

Total insured value renewable energy calculations determine the coverage limit, premium, and maximum payout available under a property insurance policy. Solar decommissioning bond requirements determine the amount of financial assurance a project owner must post to satisfy state regulatory obligations. Both numbers are downstream outputs of the same input: the value of the assets in the field, what it costs to replace them, and what they recover at end of life. When that input is inaccurate, both outputs are wrong. And in 2026, that input is moving faster than most teams are tracking.

Why These Two Instruments Share the Same Data Problem

The legal definition of how decommissioning bonds are sized makes the connection explicit.

State financial assurance requirements mandate that bond amounts must cover equipment removal, recycling costs, and site restoration, minus salvage value. A standard two-megawatt installation faces solar decommissioning costs typically ranging from $60,000 to $150,000, with figures fluctuating based on project size, location, and equipment type. (Energyscape Renewables, December 2025)

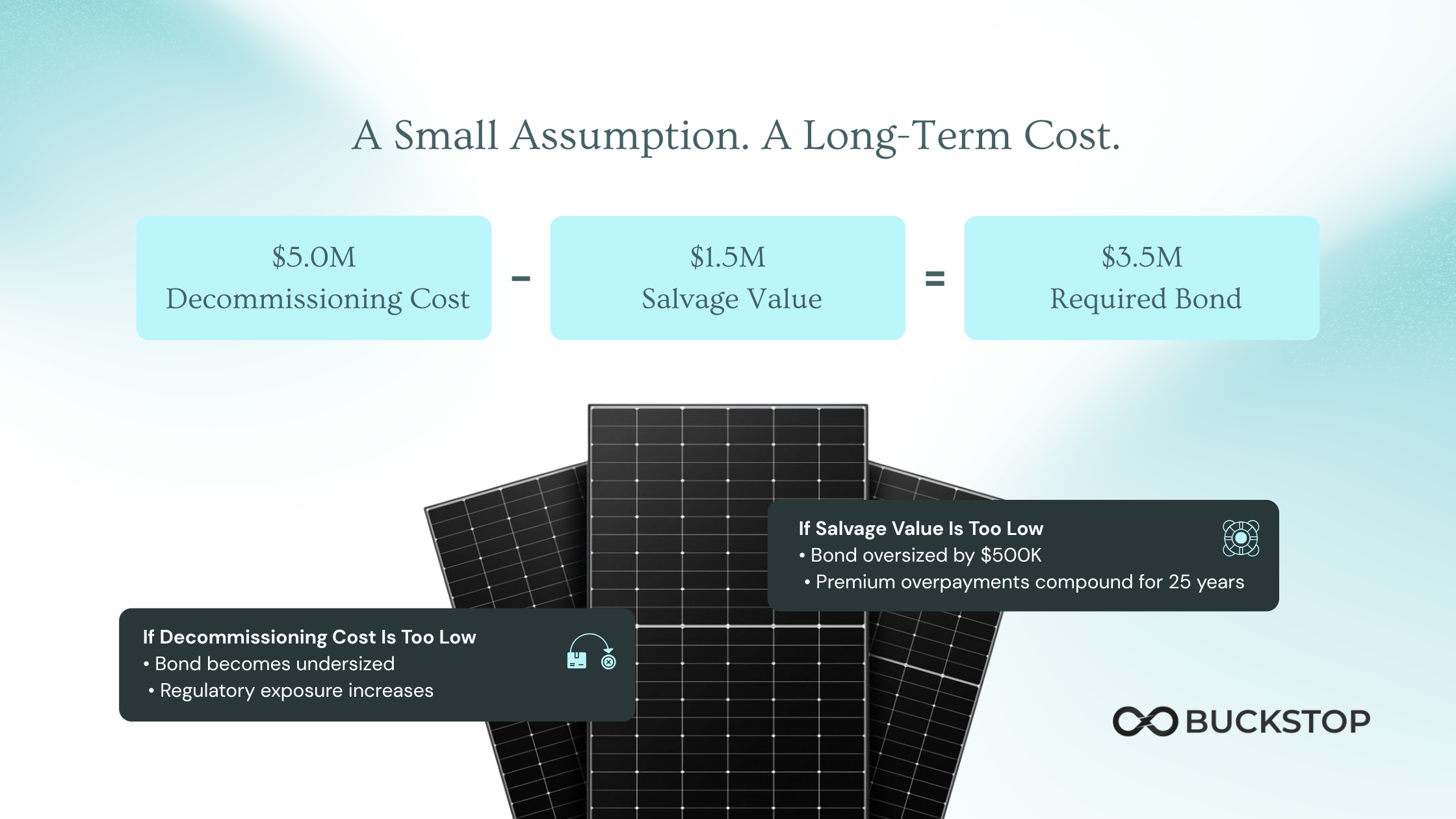

The formula is: decommissioning cost minus salvage value equals required bond amount.

The TIV formula is structurally similar: replacement cost minus salvage offset equals net insured value.

Both calculations require the same two inputs.

- Current replacement cost, which is what it costs to replace or restore the asset under current market conditions.

- Current salvage value, which is what the asset recovers across resale, recycling, and scrap pathways.

When replacement cost assumptions are stale and salvage value assumptions are generic, both instruments carry the same error in opposite directions. A stale replacement cost understates TIV and the insurance coverage attached to it. An understated salvage value overstates the bond requirement and locks up capital unnecessarily.

Most project teams do not connect these dots because the TIV is prepared by the insurance broker at policy inception and the decommissioning bond is sized by an engineer at permitting. They use different consultants, different methodologies, different assumptions, and different update cycles. The result is that both documents are wrong in correlated ways that nobody catches until a loss event, a bond dispute, or a regulatory audit makes the gap visible.

The Scale of the Regulatory Obligation

Understanding why the decommissioning bond connection matters requires understanding how rapidly the regulatory landscape has changed.

More than half of all US states had legislative action on solar and storage decommissioning in 2025, double the number from 2024. More than 35 states now have statewide solar decommissioning policies in place. (NC Clean Energy Technology Center, January 2026) In April 2025, North Carolina implemented updated utility-scale decommissioning rules applying to all new projects with nameplate capacity of 2 MW or greater. Georgia mandated decommissioning requirements starting January 2025. Texas and Oklahoma passed legislation establishing decommissioning obligations for solar facility leases.

Financial assurance requirements are rising due to inflation and higher restoration costs. States want proof that project owners can cover decommissioning costs. Solar decommissioning rules are becoming stricter and more standardized across the US, with more states moving toward statewide mandates instead of local-only rules. (GreenClean Solar, March 2026)

The financial instruments required to satisfy these obligations are substantial. Surety bonds typically cost 1% to 3% of the total bond amount. Letters of credit, by contrast, often require 100% collateral or a lien on assets, which ties up bank capacity and triggers fees or covenants. Using a surety bond in place of a letter of credit can preserve the developer's working capital and borrowing power. (United Casualty, April 2026)

For a utility-scale solar project with a decommissioning cost estimate of $5 million and a salvage value assumption of $1.5 million, the required bond is $3.5 million. The annual surety premium at 1.5% is $52,500 per year. Over a 25-year project life, that accumulates to $1.3 million in premium payments on a bond sized from a decommissioning cost estimate and salvage value assumption that may both be materially wrong.

If the salvage value is understated by $500,000 due to stale commodity price assumptions, the bond is oversized by $500,000 and the premium overpayment compounds for 25 years. If the decommissioning cost estimate is understated because replacement economics have changed since the estimate was prepared, the bond is undersized and the regulatory exposure is real.

How Commodity Price Movements Are Simultaneously Moving Both Numbers

The most immediate driver of the data gap between current instruments and current market conditions is commodity price movement. Copper hit a record $14,527 per metric ton in January 2026, a 16% rise from December 2025 alone. Silver reached an all-time high above $121 per ounce in January 2026 after gaining more than 130% during 2025. (Crux Investor, March 2026 / Investing News Network, April 2026)

These are the same materials embedded in every solar panel, inverter, and cable run in the field. Copper wiring and silver contacts in modules. Aluminum frames. Copper busbars in inverters. Every utility-scale solar project is a physical inventory of critical minerals whose market value is actively repricing. For TIV purposes, copper and silver price movements affect replacement cost calculations. The cost to replace copper cabling, aluminum racking, and module interconnects is higher today than at any point in the past three years. A TIV built on pre-2024 replacement cost assumptions is systematically understated.

For decommissioning bond purposes, copper and silver price movements directly affect the salvage value offset. The metallic content value of a utility-scale solar asset at current commodity prices is materially higher than most salvage assumptions built into existing bond calculations reflect. A bond sized on pre-2024 salvage assumptions is oversized, locking up capital the project does not need to post. Both instruments are simultaneously wrong, in opposite directions, for the same underlying reason: the commodity data has moved and neither calculation has been updated.

Texas state law now requires large-scale solar project owners to provide financial assurance in the form of a decommissioning bond to ensure that panels are not abandoned at the end of their life. Under 2026 updates, these bonds are tied to certificates of recycling provided by authorized facilities. (Okon Recycling, April 2026) When bond calculations are tied to specific recovery pathways certified by specific recyclers, the salvage value input is no longer a generic assumption. It is a transaction-backed figure that must reflect actual market pricing for those specific pathways.

What Lenders Are Missing in Their Collateral Assessment

For lenders with solar project finance exposure, the TIV and decommissioning bond connection creates a collateral assessment gap that most credit teams have not fully mapped.

At the project finance level, the lender's collateral consists of the project's physical assets, the revenue they generate, and the financial instruments that protect the value of both. TIV determines whether the insurance policy adequately covers the replacement cost of the collateral in a loss scenario. The decommissioning bond determines the financial assurance adequacy for end-of-life obligations.

Both instruments directly affect the project's financial position. An underinsured project, one whose TIV understates actual replacement cost, carries an insurance gap that reduces the collateral value available to the lender in a distress scenario. A project with an oversized decommissioning bond has locked up capital unnecessarily in a financial instrument that produces no return, reducing the project's free cash flow and potentially its debt service coverage ratio.

Lenders or financial institutions providing project financing may require decommissioning bonds as a condition for providing loans or credit to solar project developers, helping to protect their investment in case the project needs to be decommissioned. (The Horton Group) When the lender requires the bond as a condition of the facility, they are accepting the bond sizing methodology without necessarily scrutinizing the salvage value assumption underlying it. That assumption determines how much capital the project is tying up in the bond, which affects the project's liquidity and debt service capacity.

Decommissioning bonds can be very challenging to underwrite due to the length of the obligation. Solar power plants are designed for operation 25 years into the future. Therefore, to write a bond for that length of time is virtually impossible without significant collateral. Bonds to meet these requirements are either annually renewable or run for an acceptable specified period of time with renewal options. (FirstNRG) This creates ongoing exposure to bond resizing at each renewal, where changes in salvage value assumptions or decommissioning cost estimates can require the project to post significantly different bond amounts from year to year.

The lender whose credit model does not account for bond resizing risk, or whose collateral assessment does not connect TIV accuracy to salvage value methodology, is working from an incomplete picture of the project's financial risk profile.

The Solar Project Finance Collateral Gap in Practice

The connection between TIV and decommissioning bonds creates specific, quantifiable gaps in solar project finance collateral assessment that most lenders are not systematically tracking.

Gap 1: Correlated undervaluation of replacement cost

If a project's TIV was calculated at financial close using module pricing from 2022 and has not been updated, it understates current replacement cost by the amount that module prices have moved since then. US module prices rose 14% between January and November 2025. Antidumping duties of up to 3,521% on imports from four countries representing 77% of US module supply have structurally changed replacement cost economics. (US Department of Commerce, April 2025) A lender whose collateral assessment relies on a TIV built on pre-tariff pricing is overstating the insurance coverage available to protect their collateral.

Gap 2: Correlated overvaluation of bond requirement

The same project likely has a decommissioning bond sized from a salvage value estimate that predates the current commodity price environment. Copper at $14,527 per metric ton and silver at an all-time high mean the metallic content value of the project's assets is significantly higher than a 2022 or 2023 salvage assumption reflects. The bond is oversized. The project is posting more surety premium than necessary. That excess premium is a real cash cost that reduces free cash flow available for debt service.

Gap 3: Disconnected update cycles

Most state regulations require decommissioning cost estimates to be reviewed every five years. Many TIV update cycles are annual but indexed to general inflation rather than asset-specific market pricing. The result is that both documents use different assumptions updated on different schedules, producing a correlation of errors that no single advisor is tasked with identifying.

The most reasonable approach, one that protects both the project owner and the jurisdiction, is to disallow only a certain percentage of salvage value, for example 15 to 20%, while increasing the net decommissioning cost commensurately. (Surety Bond Professionals) The jurisdictional variation in how salvage value is treated in bond calculations adds another layer of complexity for lenders with multi-state portfolios. A project in a state that disallows salvage value offsets requires a larger bond than an identical project in a state that allows full offset, regardless of the actual asset value. IEA

What Transaction-Backed Residual Value Intelligence Solves

The root cause of the TIV and decommissioning bond disconnect is the absence of a shared, current, transaction-backed dataset that both instruments can draw from.

When the salvage value input in the decommissioning bond calculation and the salvage offset in the TIV calculation are both sourced from the same transaction-backed benchmark built from real observed outcomes across resale, refurbishment, recycling, and scrap pathways, the correlated errors are resolved at the source.

Buckstop's residual value indexes are built from observed market data tied to actual recovery outcomes. That data incorporates manufacturer, age, wattage, condition, configuration, and geographic and regulatory factors that influence recovery value. Commodity price movements, secondary market transaction data, and technology-specific pricing are incorporated on an ongoing basis.

For a lender evaluating a solar project's financial assurance adequacy and insurance coverage simultaneously, transaction-backed residual value intelligence provides the shared foundation that makes both assessments coherent and current. The TIV net replacement cost and the bond net decommissioning cost are built from the same dataset, updated on the same cadence, and defensible against the same level of underwriter and regulatory scrutiny.

For a project owner managing both instruments across a multi-project portfolio, the same dataset that reduces the bond requirement by accurately reflecting current salvage value also reduces the insurance premium by accurately reflecting the salvage offset in the TIV calculation. The financial benefit flows in both directions simultaneously.

The Bottom Line

The solar decommissioning bond and total insured value for renewable energy assets are not parallel workstreams. They are downstream outputs of the same upstream data: what the assets are worth, what they cost to replace, and what they recover at end of life. Most lenders, brokers, and asset managers do not treat them this way. TIV is handled by the insurance team. The bond is handled by the permitting consultant. Both use different assumptions, different methodologies, and different update cycles. Both are wrong in correlated ways that produce excess cost in the bond and excess risk in the insurance coverage simultaneously.

Solar decommissioning rules are becoming stricter and more standardized across the US. Financial assurance requirements are rising. More states are moving toward statewide mandates and recycling requirements are expanding. (GreenClean Solar, March 2026) As the regulatory environment tightens and the commodity markets reprice, the gap between stale assumptions and current market reality grows wider.

The connection between decommissioning bonds and TIV is the connection most lenders are missing. Closing it requires shared data. Transaction-backed replacement cost benchmarks and salvage value assessments built from real observed market outcomes, updated regularly, and applied consistently across both instruments.

That is how excess bond costs get recovered. That is how insurance gaps get closed. And that is how lenders get a complete picture of the financial risk profile of the assets they are financing.

Buckstop builds transaction-backed residual value intelligence for solar and BESS assets across resale, refurbishment, recycling, liquidation, and scrap pathways. Explore Buckstop Residual Value Intelligence at buckstop.

Frequently Asked Questions

What is the connection between solar decommissioning bonds and total insured value?

Solar decommissioning bonds and total insured value for renewable energy assets share the same underlying dataset: the current replacement cost of the assets and their current salvage value across recovery pathways. Bond amounts are legally defined as decommissioning cost minus salvage value. TIV net replacement cost similarly offsets gross replacement cost by recoverable salvage value. When the input data is inaccurate, both instruments carry correlated errors: TIV understates insurance coverage if replacement cost is stale, and bond requirements are oversized if salvage value is understated. Both errors compound over the project life.

How do solar decommissioning bond requirements affect project finance?

Solar decommissioning bond requirements affect project finance in three ways. First, they represent a direct capital cost through annual surety premiums of 1% to 3% of the total bond amount, which reduces free cash flow available for debt service. Second, in states that allow letters of credit in lieu of surety bonds, the LOC requirement ties up 100% of the bond amount as collateral, further constraining project liquidity. Third, bond resizing at periodic update intervals can require material changes to the project's financial assurance structure, affecting covenants and lender requirements. Lenders that require decommissioning bonds as a condition of the facility accept the bond sizing methodology without scrutinizing the salvage value assumptions underlying it.

Why are solar salvage value assumptions in decommissioning bonds frequently wrong?

Solar salvage value assumptions in decommissioning bonds are frequently wrong because they are based on estimates prepared at permitting using static consultant reports that do not update with commodity price movements or secondary market conditions. Copper at $14,527 per metric ton and silver at an all-time high above $121 per ounce mean that the metallic content of deployed solar assets is worth materially more today than pre-2025 salvage assumptions reflect. Most state regulations require decommissioning cost estimates to be reviewed only every five years, which is not adequate for maintaining accuracy in a market where commodity prices can move 16% in a single month.

What is the decommissioning bond cost for a utility-scale solar project?

The decommissioning cost for a standard 2 MW solar installation typically ranges from $60,000 to $150,000 before salvage value offset, depending on project size, location, and equipment type. The required bond amount equals that decommissioning cost minus allowable salvage value. Annual surety bond premiums are typically 1% to 3% of the total bond amount. For a $3 million net bond requirement, that represents $30,000 to $90,000 in annual premium. Over a 25-year project life, the cumulative premium is significant. Accurately sizing the bond through defensible salvage value analysis directly reduces both the bond amount and the annual premium.

How do state decommissioning regulations differ in their treatment of salvage value?

State treatment of salvage value in decommissioning bond calculations varies significantly. Some jurisdictions allow full offset of estimated salvage value against decommissioning cost. Others disallow a percentage of salvage value, typically 15% to 20%, to provide a buffer against market volatility. A small number require full gross-cost bonding regardless of salvage value. This variation means that a project with identical assets in different states may have materially different bond requirements. Lenders with multi-state solar portfolios need to map the salvage value treatment in each jurisdiction and understand how commodity price movements affect bond sizing under each state's specific calculation methodology.

How often should TIV and decommissioning bond calculations be updated?

Given current market conditions, both TIV and decommissioning bond inputs should be reviewed annually at minimum with specific attention to commodity price movements, module pricing by technology type, and secondary market transaction data. Many states require decommissioning cost estimates to be updated every five years, which is not adequate for bond sizing purposes in a market where copper rose 16% in a single month and module prices moved 14% in a single year. For lenders with project finance exposure to large solar portfolios, annual reconciliation of TIV and decommissioning bond calculations against the same transaction-backed dataset is the appropriate standard.