.png)

Stop guessing on residual risk. Start pricing with intelligence.

Many underwriting decisions still rely on conservative defaults, static depreciation curves, or manual spreadsheets that are hard to defend under scrutiny. The result is over-bonding, excess capital lock-up, and avoidable loss exposure.

Buckstop brings transaction-backed intelligence into underwriting decisions before risk is bound and before claims occur.

The Cost of Manual and

Assumption-Led Underwriting

Excess capital

lock-up

Conservative assumptions inflate bond sizes, premiums, and limits, tying up capital for both insurers and policyholders.

Missed recovery value

Assets written off as “junk” often hold meaningful recoverable value that never gets priced into claims outcomes. Without a defensible benchmark, underwriting defaults to caution instead of accuracy.

Defensibility gaps

Manual spreadsheets and static curves often fail reinsurer, syndicate, or internal review when assumptions are challenged.

The Core Underwriting Question

Are we pricing this risk correctly and can we recover value if something goes wrong?

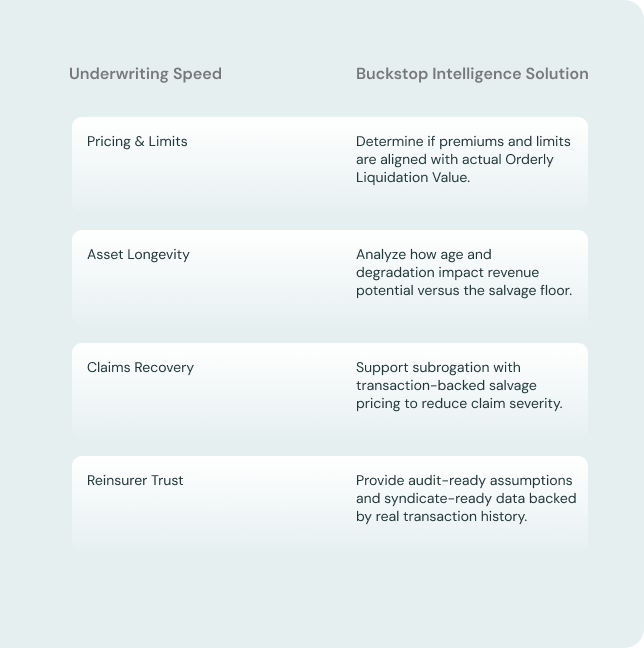

Underwriting Speed

Buckstop Intelligence Solution

Pricing & Limits

Determine if premiums and limits are aligned with actual Orderly Liquidation Value.

Asset Longevity

Analyze how age and degradation impact revenue potential versus the salvage floor.

Claims Recovery

Support subrogation with transaction-backed salvage pricing to reduce claim severity.

Reinsurer Trust

Provide audit-ready assumptions and syndicate-ready data backed by real transaction history.

Built for Speed & Accuracy

"What used to take weeks of analyst effort now runs

in minutes.” - Policy Underwriter based in Texas

Upload entire portfolios via Excel or structured files for instant benchmarking.

Use our API to feed valuation inputs directly into your existing underwriting workflows.

Instantly validate manufacturer, age, and wattage data against real market outcomes.

The "Secret Sauce": The Buckstop Index

Our platform is powered by a proprietary residual value index built on real-world resale and scrap transactions. This ensures:

single-point guesses; provide a

range of outcomes based on data.

Reducing Net Claims Payouts Through Salvage Intelligence

Buckstop helps insurers

- Identify recoverable value in damaged or impaired assets

- Support subrogation with transaction-backed salvage pricing

- Reduce claim severity by quantifying realistic recovery outcomes

How Buckstop Supports Underwriting Teams

Teams use Buckstop to

- Price decommissioning and salvage exposure using real transaction data

- Benchmark risk automatically from schedule of values data such as manufacturer, age, and wattage

- Validate recovery assumptions across resale, recycling, and scrap pathways

- Quantify downside risk through scenario and sensitivity analysis across loss events

- Reduce underwriting cycle time by replacing repeated manual valuation work with automation

Built to Save Time for Underwriters

Buckstop removes manual bottlenecks by supporting

Bulk asset uploads via Excel or structured files

Bulk asset uploads via Excel or structured files- API-based valuation inputs into underwriting workflows

- Repeatable reporting across policies, portfolios, and renewals

A Loss Control Layer Underwriters Can Defend

Buckstop functions as a loss control and decision-support layer by providing

backed by real

transaction history

rather than single-point

assumptions

to data recency and

coverage

for reinsurers, regulators,

and internal review

Index-Backed,

Not Assumption-Driven

At the core of Buckstop is a residual value index built on real resale and scrap transactions. This index powers underwriting decisions with.

- Defensible value ranges

- Scenario and sensitivity modeling

- Consistent application across policies, claims, and portfolios

The same benchmark applies across underwriting, claims, and renewals. No rework. No assumption drift. Reduce residual value risk before it hits your loss ratio.