.png)

When capital is on the line, assumptions are not enough

Capital and financing decisions break down when residual value assumptions are weak.

The Decision That Matters

What is this asset actually worth at exit, default, or decommissioning?

Capital providers need to understand

How much value can be recovered in real markets

How much value can be recovered in real markets- Whether residual value assumptions support financing terms

- How downside exposure changes due to channel and timing

- Whether capital is being over- or under-protected

How Buckstop Supports Investment Decisions

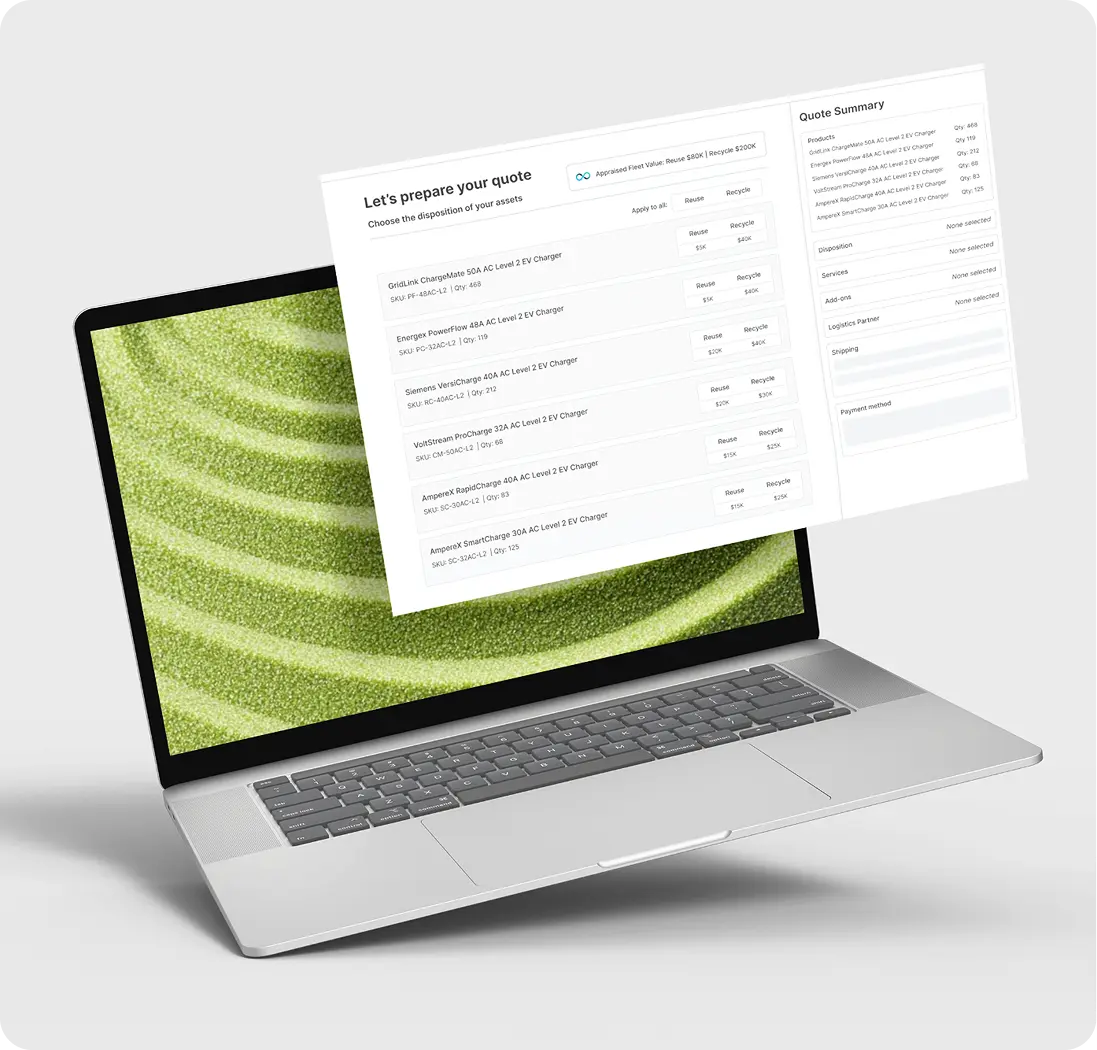

Buckstop uses residual value indexes and automated reporting to anchor financing models in real transaction outcomes.

Using Buckstop, teams can

- Validate residual value assumptions used in financing

- Stress-test downside exposure across resale, recycling, and scrap

- Quantify capital at risk under different scenarios

- Replace one-off valuation work with repeatable analysis

This allows capital decisions to be based on evidence, not optimism or fear.

Decisions Buckstop Helps Answer

Are residual value

assumptions strong enough

to support this financing structure?

assumptions strong enough

to support this financing structure?

How much capital is

actually exposed at

end- of- life or default?

actually exposed at

end- of- life or default?

Are decommissioning and recovery costs over- or under-estimated?

Would a change in timing

or pathway materially

impact exit value?

or pathway materially

impact exit value?

Is capital being locked up

unnecessarily due to

conservative assumptions?

unnecessarily due to

conservative assumptions?

Each of these decisions depends on understanding value before action is taken.

Built on Residual Value

Indexes, Not One-Off Analysis

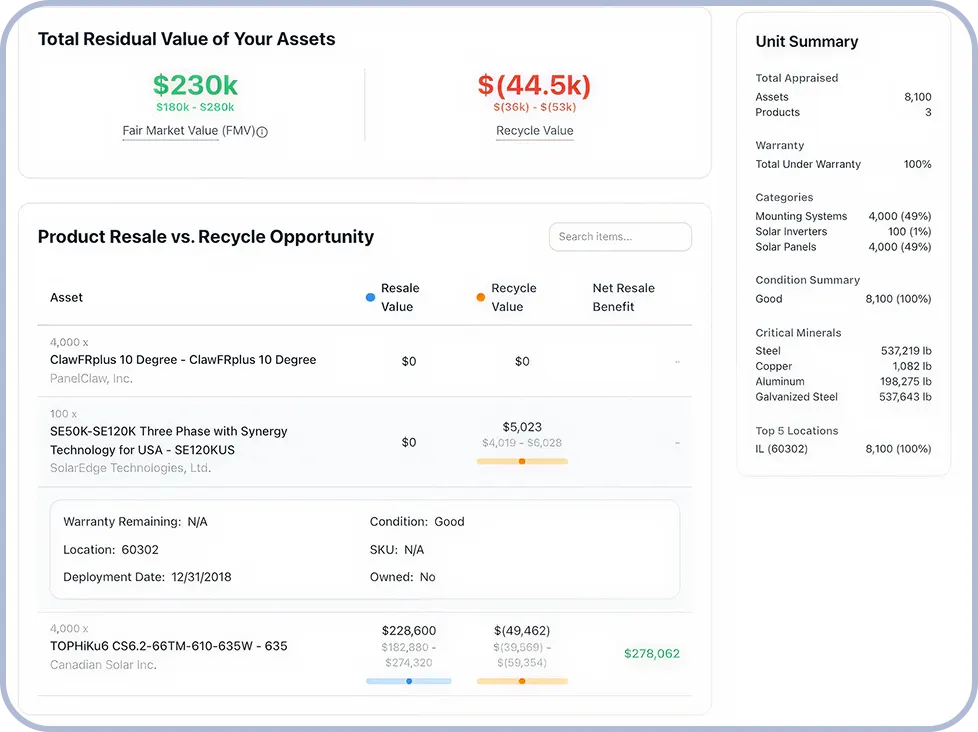

At the core of Buckstop is a residual value index that captures real transaction outcomes across resale and scrap markets.

That index powers automated reports designed for capital and finance teams, including:

- Transaction-backed value ranges, not point estimates

- Confidence scoring based on data breadth and recency

- Scenario and sensitivity analysis tied to timing and regulation

- Audit-ready assumptions suitable for credit committees and risk review

The same benchmark can be applied consistently across portfolios and deals.

Frequently Asked Questions

Why are residual value assumptions the weakest link in solar financing today?

How does post-PPA revenue dependency change how lenders assess residual value?

Could you please clarify what credit committees require before they approve residual value assumptions?

How does Buckstop protect capital when book value and real market value are disconnected?

Can residual value intelligence reduce bond sizes without increasing risk exposure?

How should financing teams stress-test residual value assumptions before a deal closes?

Is Buckstop useful for refinancing or only for structuring new deals?