.png)

Common Mistakes in Infrastructure Valuation Models That Distort Returns

Infrastructure valuation models are designed to look precise. But precision in format does not mean accuracy in outcome. Across project finance and energy infrastructure, the same pattern repeats. Models hold up under internal review but break at exit, refinancing, or impairment.

Residual value assumptions determine bond sizing, financing terms, recovery outcomes, and exit risk. Yet most teams still rely on spreadsheets, static studies, or conservative guesswork. When those assumptions are wrong, the distortions compound across a 2530-year asset life and surface as deal-breaking surprises at exactly the moment when there is no time to fix them.

1. Residual Value Assumptions Disconnected from Market Reality

Residual value modelling in infrastructure is where optimism bias does the most systematic damage. The gap between assumption and market reality surfaces a decade later, at exactly the moment when time-sensitive decisions about repowering, retirement, or refinancing cannot wait.

Mistake: Using book value as a proxy for residual value

Straight-line depreciation schedules are an accounting convention. They are not a real-world representation of physical asset condition, market realisable value, or what a secondary market buyer will actually pay. A solar panel, a wind turbine, or a water treatment facility degrades according to engineering and market curves, not a 20-year amortisation table.

The gap between book value and genuine market residual value is substantial and it has real consequences. Teams routinely write assets off at zero when meaningful resale recovery remains. Others overstate residual value in financing models, creating exposure that surfaces under audit, during M&A, or at refinancing.

The fix: Residual value needs to be grounded in real transaction data, not depreciation schedules. Buckstop's Solar Residual Value Index tracks actual scrap and resale outcomes from historic and current transactions, giving teams a continuously refreshed benchmark that reflects what assets genuinely trade at in secondary markets, not what the accountant's schedule says they should be worth.

Mistake: Single-point residual value estimates with no range or confidence interval

A single residual value number hides assumptions. It tells you nothing about downside exposure, nothing about what the P10 outcome looks like under adverse market conditions, and nothing about which factors drive the most variance. Yet single-point estimates are the standard output from consultant reports and most internal models.

This is particularly acute in energy infrastructure valuation, where technology evolution, commodity price shifts, and policy changes mean residual value ranges can be wide. A point estimate obscures all of that and makes it structurally impossible to size bonds, reserves, or recovery provisions correctly.

The fix: Buckstop outputs transaction-backed value ranges, not single numbers. Teams get a full distribution of outcomes with explicit assumptions, confidence scoring, and audit-ready documentation that holds up to risk committee and regulatory scrutiny.

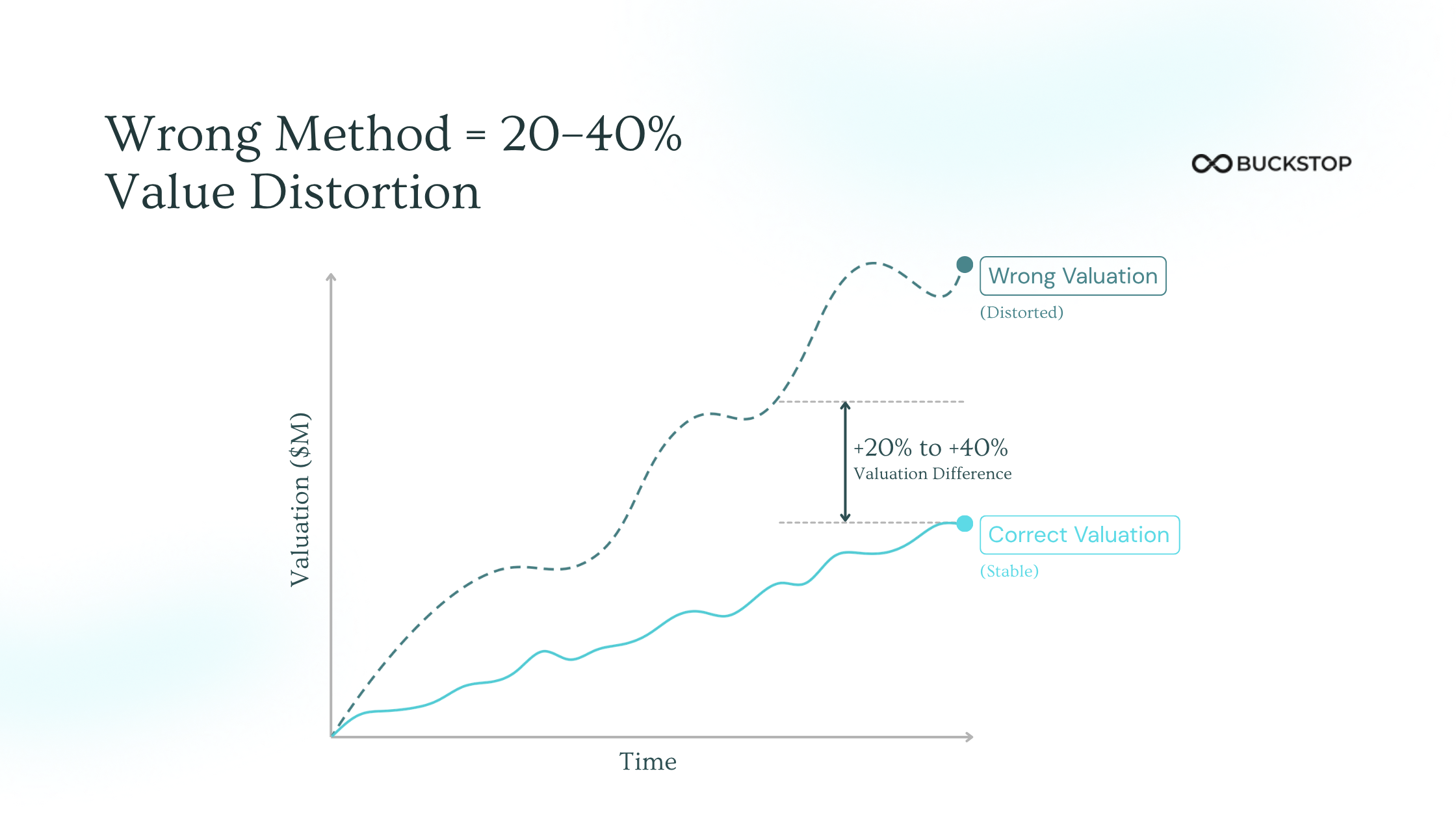

2. Terminal Value Methodology Mismatch

Terminal value infrastructure assets present a genuine methodological challenge. The right approach depends on whether the asset has a concession end date, an indefinite operating licence, a regulated asset base, or a merchant revenue profile. Using the wrong methodology can swing total equity value by 20 to 40%, and the error is often invisible until exit.

Mistake: Applying EV/EBITDA exit multiples to assets with defined end lives

A renewable energy asset approaching end-of-life or concession expiry does not have terminal value in the traditional sense. Applying an EV/EBITDA exit multiple implies a buyer at exit who will pay for a perpetuity that does not structurally exist. The model is wrong on first principles.

This error is common when analysts port M&A templates into project finance contexts without adjusting for the fundamental difference between fee simple ownership and time-limited rights, or between an operating asset and one approaching transition.

The fix: For assets approaching end-of-life or concession expiry, terminal value should be modelled as remaining cash flows plus realistic recovery value at exit. That recovery value must be grounded in actual secondary market data, not accounting residuals or a consultant's stale one-off estimate.

Mistake: Perpetuity growth rate inconsistent with contract or regulatory structure

Even for long-lived assets, the Gordon Growth Model perpetuity assumption needs to be anchored to something real. A solar asset with revenue capped by a fixed PPA cannot defensibly assume a 2.5% long-run nominal growth rate. Neither is applying GDP growth to assets with declining technology value curves or real-terms revenue erosion baked into the contract.

The fix: Derive your long-run growth rate from the actual contract escalation mechanism, the regulatory determination, or independent sector forecasts. Make it explicit, documented, and sensitivity-testable. If the assumption cannot survive scrutiny by an auditor or counterparty, it should not be in the base case.

3. Discount Rate Construction Errors

The discount rate in infrastructure financial modelling is doing a lot of work. It needs to reflect the specific risk profile of the specific asset at its specific lifecycle stage. A rate lifted from a Bloomberg comparables screen or taken from a benchmarking report covering a heterogeneous sector basket is unlikely to be right.

Mistake: Applying a flat WACC across assets with changing risk profiles over time

An operational energy asset in steady-state revenue generation carries categorically different risk from that same asset in its final years, when technology obsolescence, repowering decisions, and end-of-life residual value uncertainty dominate the picture. A model that applies the same discount rate across a 25-year project life conflates meaningfully different risk periods.

The fix: Use phase-specific discount rates or adjust the risk premium explicitly at major lifecycle transitions. End-of-life uncertainty and residual value dispersion both justify a higher rate in the terminal period. Buckstop's scenario modelling provides explicit uncertainty ranges around residual value that inform how much additional risk premium is warranted rather than leaving it to assumption.

Mistake: No sensitivity testing on the discount rate against residual value interactions

When a large share of value sits in terminal or residual assumptions, the interaction between the discount rate and residual value becomes the dominant driver of IRR. Models that sensitivity-test revenue or cost assumptions but leave the discount rate and residual value static in every scenario are missing the most important variable combination.

The fix: Always run a two-dimensional sensitivity grid: discount rate versus residual value. Make sure the investment case holds in the quadrant where both move adversely. If it does not, that is the risk the capital structure needs to price.

4. Mispriced Recovery Value Assumptions in Infrastructure

Recovery value assumptions are chronically underbuilt across infrastructure financial modelling. Most models either ignore them entirely, treat them as negligible, or use a round-number percentage of original cost that has no connection to actual secondary market behaviour.

"Our books showed zero value and pointed to disposal. Buckstop uncovered remaining resale potential, helping us recover meaningful capital instead of scrapping." — Portfolio Finance Manager, Renewable Energy Operator

Mistake: Writing recovery value to zero without secondary market analysis

For many energy infrastructure asset classes, meaningful resale value exists in secondary markets well beyond the point where book value hits zero, particularly for components with reuse, refurbishment, or repowering potential.

Teams that write recovery value to zero are systematically leaving capital on the table. They are also mispricing decommissioning bonds, over-reserving for disposal costs, and producing financing structures that are larger than they need to be.

The fix: Recovery value assumptions need to be grounded in actual secondary market transaction data for comparable asset classes, vintages, and conditions. Buckstop's platform surfaces 20 to 25% resale recovery that traditional spreadsheet models write off entirely as scrap. That is not a rounding error. It is capital that should be informing bond sizing, exit strategy, and asset management decisions.

Mistake: Not distinguishing resale value from scrap or recycling value

Resale value and scrap or recycling value are different numbers with different market dynamics, different buyer pools, and different optimal timing windows. Models that collapse these into a single salvage value line are structurally unable to inform the most valuable end-of-life decision: whether to resell, repower, or recycle, and when.

The fix: Model resale and recycling pathways separately with explicit market anchoring for each. Buckstop provides pathway-specific recovery and liquidation intelligence to support this decision rather than defaulting to disposal.

7. The Static Model Problem

Most organisations answer residual value questions using one-off consultant reports that quickly become obsolete, spreadsheets with single points of failure, and assumptions disconnected from real transactions. The consequences are predictable: recovery value is left on the table, decommissioning risk is mispriced, bonds and financing are incorrectly sized, and hidden costs surface during M&A, exits, defaults, or audits.

Buckstop's positioning is direct on this: consultants deliver static answers, Buckstop establishes a living benchmark. Spreadsheets hide assumptions, Buckstop exposes them. Reporting tools document outcomes, Buckstop informs decisions before outcomes are locked.

That distinction matters for any team whose decisions are accountable to risk committees, auditors, and capital providers who will ask hard questions about the foundation of the numbers.

How Infrastructure Valuation Models Need to Evolve

The shift is not toward more complex models.

It is toward better inputs.

Effective infrastructure asset valuation requires:

- Transaction-backed recovery data, not static assumptions

- Scenario-based modelling, not single-point estimates

- Net recovery analysis, including decommissioning costs

- Traceable assumptions, linked to real benchmarks

This is where platforms like Buckstop are changing infrastructure valuation workflows.

Instead of assigning residual value, they anchor it to:

- Real transaction data

- Indexed recovery outputs

- Scenario-based modelling across market conditions

So valuation becomes measurable, defensible, and aligned with actual market behaviour.

FAQs

What are infrastructure valuation models?

Infrastructure valuation models are financial models used to estimate the value of long-term assets such as energy projects, transport systems, or industrial infrastructure based on projected cash flows, terminal value, and risk assumptions.

Why is residual value important in infrastructure valuation?

Residual value can contribute a significant portion of total asset value, often between 20% and 50%, especially in long-duration projects. Incorrect assumptions can materially distort IRR and debt sizing.

What is the biggest mistake in infrastructure financial modelling?

The most common mistake is relying on unsupported residual value assumptions without linking them to actual recovery market data or running proper sensitivity analysis.

How do decommissioning costs affect infrastructure valuation?

Decommissioning costs can significantly reduce or eliminate recovery value. In some cases, they can exceed salvage value, resulting in negative terminal outcomes.

How can infrastructure valuation models be improved?

Models can be improved by using transaction-backed data, scenario-based recovery modelling, and ensuring all assumptions are traceable and defensible.