.png)

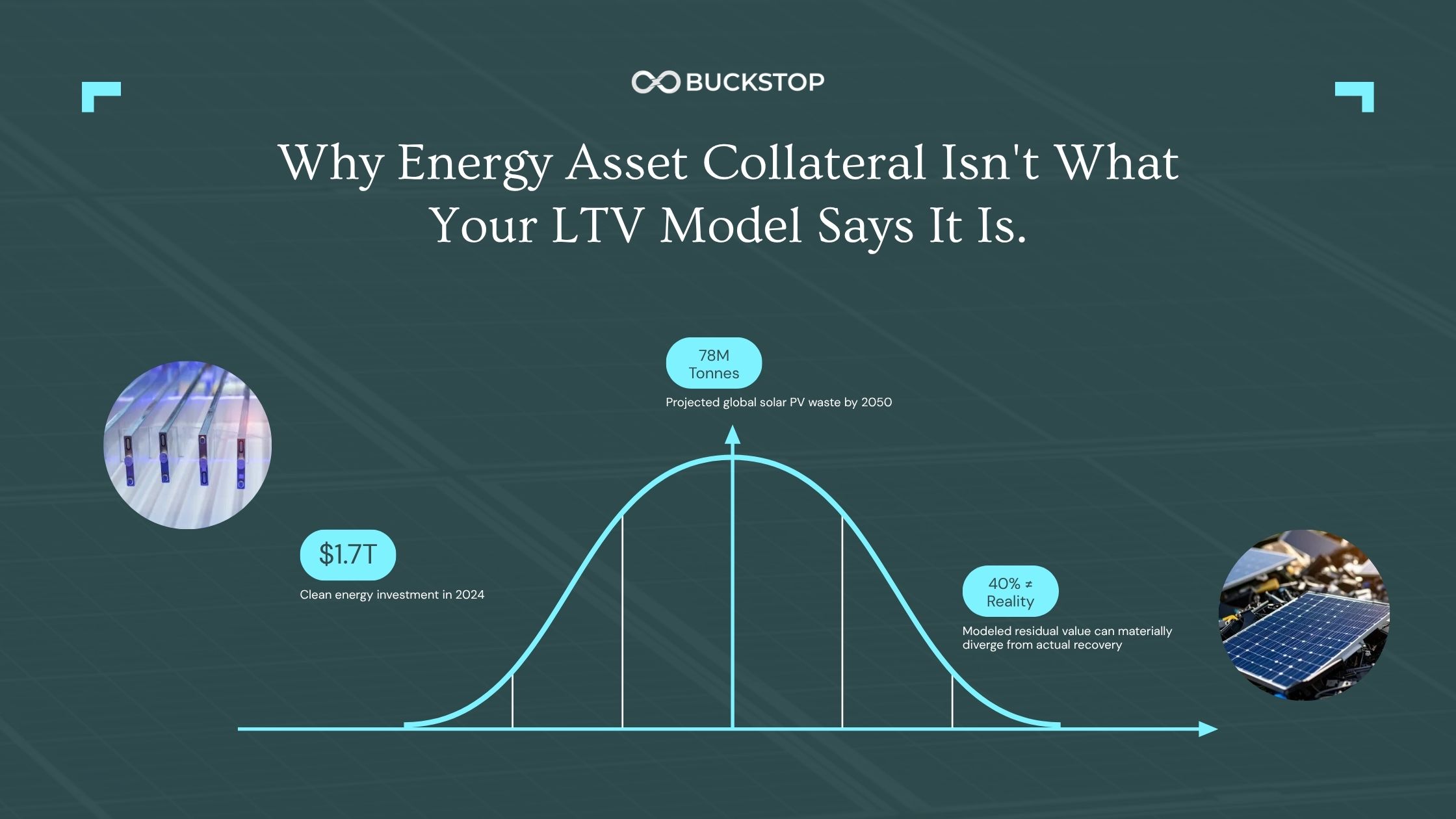

Why Energy Asset Collateral Isn't What Your LTV Model Says It Is

For years, renewable infrastructure lending operated on a simple assumption: if the project generated stable cash flow and maintained healthy debt service coverage, the collateral behind the loan would hold its value. That assumption shaped how lenders approached LTV energy infrastructure models across solar, storage, and broader energy portfolios. But the market is changing.

Across renewable finance, lenders are realising that energy asset collateral value often looks very different in reality than it does inside an underwriting model. Particularly once projects age, refinancing becomes difficult, or a default forces lenders to recover value from the underlying asset. The issue is not that LTV models are flawed. The issue is that many still rely on static depreciation assumptions that fail to reflect how energy assets behave in real-world secondary markets.

Why Traditional LTV Energy Infrastructure Models Are Breaking

Most energy project finance LTV underwriting models were built during a period of aggressive renewable deployment, low interest rates, and optimistic growth assumptions. Underwriting focused heavily on operational performance and DSCR stability while collateral assumptions became secondary. That approach worked when projects were relatively new.

It becomes riskier once those same assets age into maturity. A solar farm financed in 2016 may still appear healthy from a book value perspective while carrying materially weaker recovery potential underneath. Module degradation, declining equipment demand, freight costs, disposal obligations, and repowering economics all influence what the asset could actually recover in a distressed scenario.

That creates growing renewable energy project finance collateral risk for lenders relying on outdated recovery assumptions. According to BloombergNEF, global clean energy inestment surpassed $1.7 trillion in 2024. At the same time, the industry is entering a phase where large volumes of first-generation renewable assets are beginning to age simultaneously. That shift is forcing lenders to reevaluate how lenders value ageing energy assets beyond theoretical depreciation curves.

The Hidden Gap Between Book Value and Residual Value in Energy Assets

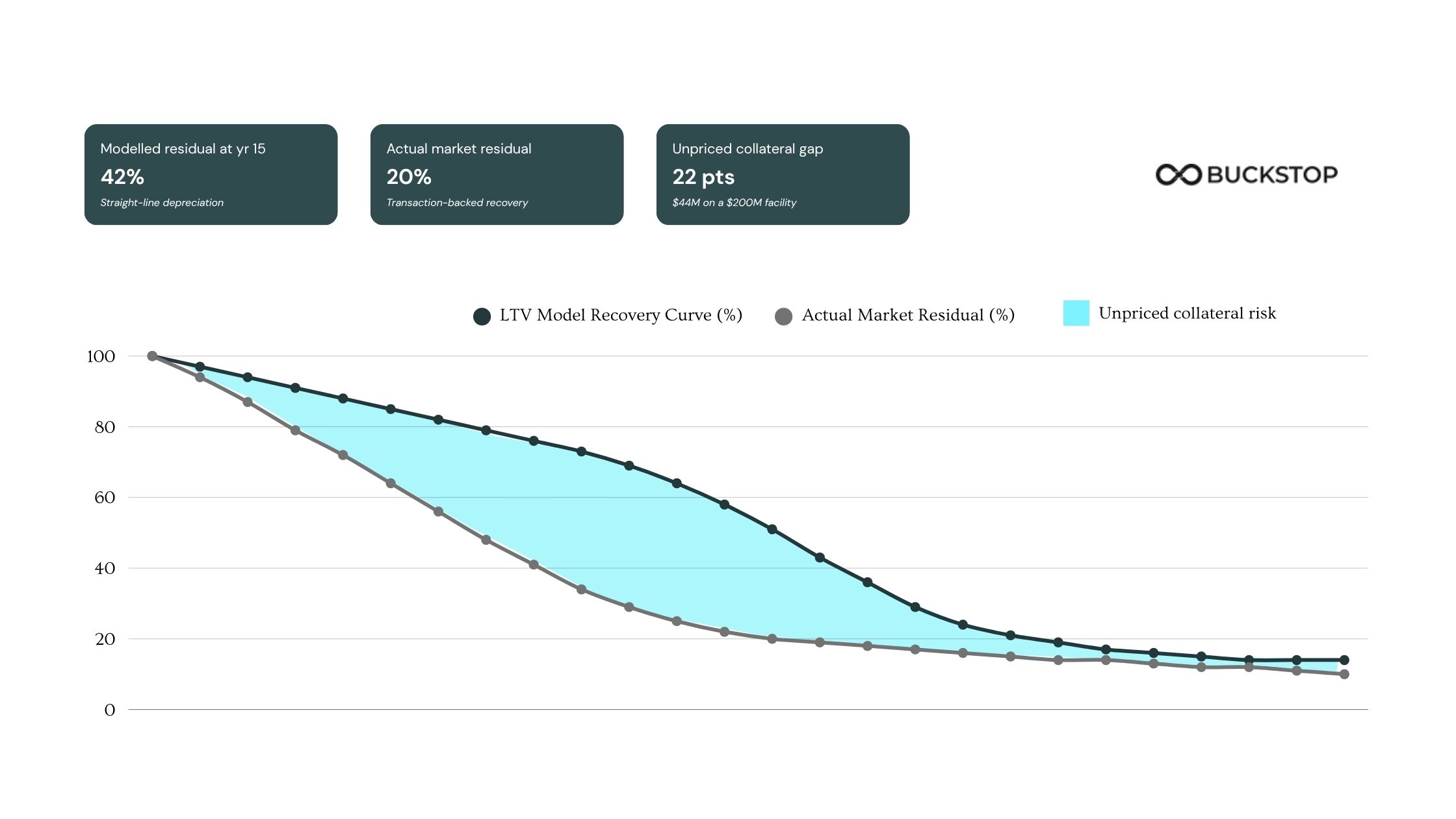

One of the biggest underwriting blind spots today is the difference between book value and residual value. Book value reflects accounting treatment. Residual value reflects market reality. Those numbers are often far apart.

An energy asset may still carry meaningful value on a balance sheet while its actual resale or recovery potential has deteriorated due to falling secondary market demand or changing technology economics. This becomes especially important in solar asset recovery rate default scenarios.

Many older solar assets were financed under assumptions that long-term recoverability would remain relatively stable. But rapid technology improvements and falling equipment prices have changed the economics of aging infrastructure. In many cases, installing new equipment is now more attractive than refurbishing older systems. That directly impacts energy asset end-of-life value. A lender may believe a portfolio retains 40% residual value based on model assumptions while actual recovery outcomes, after transportation, dismantling, labor, and resale friction, are materially lower.

This is why infrastructure lenders are paying closer attention to transaction-backed residual value intelligence instead of relying solely on static depreciation schedules.

How Lenders Value Solar Assets During Default Scenarios

When projects default, the market exposes weaknesses inside traditional underwriting assumptions very quickly. Two solar projects with similar operational performance may produce completely different recovery outcomes depending on geography, equipment quality, interconnection rights, and resale demand.

That is changing how lenders assess solar asset collateral. Sophisticated infrastructure lenders are now evaluating recovery pathways more granularly. Instead of assigning a flat recovery percentage across an entire portfolio, they are analyzing resale markets, refurbishment potential, recycling economics, and asset-specific liquidation scenarios.

The reason is simple.

Infrastructure loan collateral at maturity is becoming harder to predict. According to the National Renewable Energy Laboratory, global solar PV waste could exceed 78 million metric tonnes by 2050. As more renewable assets reach end-of-life simultaneously, recovery values may compress further due to increasing supply pressure in secondary markets.

That creates meaningful downside exposure for lenders using outdated collateral assumptions in solar project LTV underwriting. Because during distress, the market does not care what the original underwriting model projected. It cares what the asset can realistically recover today.

Why DSCR vs LTV Renewable Energy Metrics Tell Different Stories

One of the biggest misconceptions in renewable infrastructure finance is assuming a strong DSCR automatically validates collateral quality. It does not.

DSCR measures operational cash flow performance. LTV measures downside protection. A project can maintain healthy debt service coverage while the underlying collateral value weakens underneath. That distinction is becoming increasingly important as renewable infrastructure portfolios mature. Particularly in solar and storage assets where technology cycles move faster than traditional infrastructure depreciation schedules.

The DSCR vs LTV renewable energy conversation is evolving because lenders are recognizing that operational performance alone does not eliminate collateral risk. As financing conditions tighten and refinancing becomes more difficult, infrastructure debt providers are placing greater emphasis on understanding actual recovery potential under stress scenarios.

How Buckstop Helps Lenders Assess Energy Asset Collateral Value

This is where Buckstop’s residual value intelligence becomes important.

Instead of relying solely on accounting schedules or generalised engineering assumptions, Buckstop helps lenders and infrastructure finance teams evaluate energy asset collateral value using transaction-backed residual value data. That includes visibility into resale pathways, refurbishment economics, recycling value, commodity-linked recovery potential, and real-world end-of-life market behaviour.

For lenders managing renewable energy project finance collateral risk, this creates a more defensible understanding of infrastructure loan collateral at maturity. Because the difference between the modelled value and the actual recoverable value can materially impact refinancing assumptions, portfolio risk exposure, and underwriting decisions. As infrastructure markets mature, residual value intelligence is becoming increasingly important not only during distressed scenarios but also during origination itself. The lenders adapting fastest are the ones treating collateral value as a live market variable instead of a static assumption inside an underwriting spreadsheet.

The Future of Solar Project LTV Underwriting

The future of solar project LTV underwriting will likely move away from static recovery assumptions toward dynamic residual value analysis. Infrastructure lenders are beginning to integrate scenario-based recovery modelling directly into underwriting decisions. Instead of relying purely on depreciation schedules, they are evaluating how real-world market conditions could impact collateral recoverability over time. That shift matters because the biggest collateral risk in renewable infrastructure today is not necessarily project failure.

It is lenders believing the asset is worth substantially more than the market will ultimately pay for it. And as more renewable assets age into maturity, understanding how lenders value aging energy assets will become central to infrastructure credit strategy.

FAQs

Why do LTV models overstate energy asset value?

Many LTV models rely on static depreciation schedules and generalized recovery assumptions that fail to reflect real-world resale demand, technology obsolescence, disposal costs, and secondary market liquidity.

How do lenders assess solar asset collateral?

Sophisticated lenders increasingly use transaction-backed recovery analysis that evaluates resale pathways, refurbishment potential, recycling economics, and real-world market demand.

What is collateral risk in infrastructure debt?

Collateral risk refers to the possibility that an infrastructure asset recovers materially less value than expected during refinancing, distress, or liquidation scenarios.

What is the difference between book value and residual value in energy assets?

Book value reflects accounting depreciation while residual value reflects what the asset can realistically recover through resale, refurbishment, recycling, or liquidation pathways.